Iran sanctions move hits European firms

AFP/Paris

US President Donald Trump’s decision to pull the US out of the 2015 nuclear accord with Iran and reimpose a raft of sanctions puts European businesses on the spot.

While the European Union insists it will stick by the nuclear accord to allow trade to continue with Iran, European companies are wary of being caught out by the US sanctions regime and many have already cut back their presence.

The sanctions introduced in August spooked the major automakers who were already cautious about their future in Iran and mindful of their much bigger business interests in the US.

Germany’s Daimler, which was teaming up with two Iranian firms to assemble Mercedes-Benz trucks, said it had decided against going ahead.

Volkswagen had said last year it planned to resume business after a 17-year break but was very guarded in response to the latest US decision.

VW “conforms with all the applicable national and international laws and regulations concerning exports,” a spokesman said.

French automakers Renault and PSA, who make nearly half the cars sold in Iran, were cautious.

PSA, behind the Peugeot, Citroen and Opel brands, said in June it was preparing to suspend activities in Iran.

Renault says it intends to keep its activities in Iran but stands ready “to reduce the scale very sharply” if need be.

Aviation saw large contracts reached following the 2015 nuclear accord as Iran set about modernising an ageing fleet.

Airbus booked deals for 100 jets and was looking forward to many more.

However, the potential loss of business in Iran would not weigh overly heavily on Airbus given its total outstanding order book of some 7,168 planes at end-June.

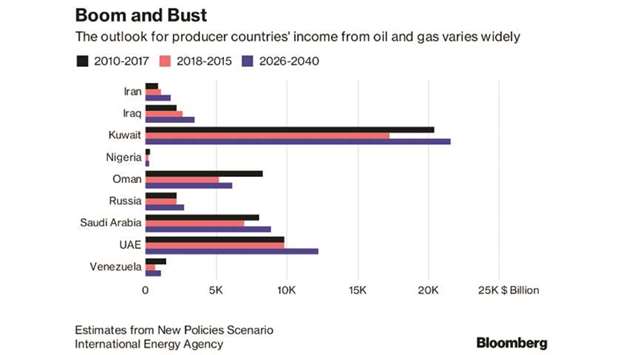

Oil is the key issue with global implications for all concerned as Washington aims to cut off Iran’s key source of foreign income.

French energy giant Total announced in August it was pulling out of a massive natural gas project.

Italian energy giant ENI meanwhile has a contract to take 2mn barrels of oil per month which it will not renew after it finishes this year.

German engineering giant Siemens signed a contract in 2016 to supply gas turbines to Iranian company Mapna.

A spokesman told AFP the company “will take the appropriate measures to bring its affairs into conformity with the multilateral framework concerning Iran.”

Italy stands to lose most in these sectors, national railway operator Ferrovie dello Stato Italiano having signed a deal in 2017 to build a high-speed line linking Qom to Arak in northern Iran.

Shipmaker Fincantieri, engineering firm Maire Tecnimont and gas boiler maker Immergas all signed a string of deals with Iran which are also threatened.

Italy was Iran’s largest European trade partner in 2017, with its exports rising 12.5% to €1.7bn.

Iran is potentially a major tourist destination but European companies were quick to pull back after the August US announcement.

British Airways and Air France halted services in September, saying the flights were not commercially viable.

German carrier Lufthansa, Austrian Airlines and Alitalia for the moment continue flights to Tehran.

French hotel chain AccorHotels, which opened an establishment in Iran in 2015, declined to comment on its plans for the future.

Spain’s Melia Hotels International chain, which signed a 2016 deal to run a five star hotel in Iran, the Gran Melia Ghoo, said in November it was still going ahead.