These are truly historic times for the Eastern Mediterranean. The region still has more than its share of problems, but we could be on the verge of a new era – and the energy industry is well-positioned to show the way.

Energy is the lifeblood of modern economies, and all of the science points to massive reserves of oil and (especially) natural gas off the coasts of several Eastern Med countries, including Cyprus, Egypt, Israel, and Lebanon. If responsibly managed, this resource will contribute both directly and indirectly to significant GDP growth, giving these countries the capacity to make long-overdue investments in education, healthcare, infrastructure, transport, and other sectors. In turn, these investments will improve overall competitiveness, raise standards of living, reduce poverty, and set the stage for self-sustaining growth over the long term.

For our region, though, “responsibly managed” means more than just following international business, governance, environmental, and safety standards: it also means finding a way to build and maintain economic and political trust, both between nation-states and within individual societies. Whether we like it or not, we are all partners in this endeavor, so we share an interest in achieving the kind of stability that encourages private investment, reduces trade barriers, and accelerates economic activity across the board. If long-time rivals provide sufficient political and/or diplomatic space for our emerging energy industry to take root, the resulting economic benefits will flow to all concerned, alleviating many of the symptoms – and even some of the causes – of the region’s various problems.

No discussion of this topic is complete without emphasizing the central role to be played by Cyprus. Although every country involved will retain some of its gas production for domestic use, for most of us the real game-changer will be a massive boost in export revenues. There are two ways to get gas to markets in Europe and elsewhere – pipelines and liquid natural gas (LNG) carriers – and Cyprus is clearly the best gateway for both.

Its geographical location, ample coastline, and unique geostrategic position make it: 1) the perfect collection and distribution point for the output of neighbors like Lebanon and Israel; 2) an ideal terminus for one or more pipelines to Turkey and the European mainland; 3) the only viable location for a regional LNG plant; and 4) a natural middleman between regional governments whose relationships are troubled or non-existent. Because of these and other qualities, including its membership in the European Union, Cyprus should be the cornerstone on which the entire edifice of regional energy growth is built.

What is more, the Republic of Cyprus (ROC), has taken serious steps to make the most of these circumstances by establishing a presence at several steps along the region’s energy value chain. It has moved quickly and effectively to make the island an indispensable regional energy hub by passing suitable legislation, setting up a national energy company, and drawing up a world-class regulatory regime. It also has already signed EEZ delimitation agreements with Egypt, Lebanon and Israel, attracted oilfield support, communications, and other service firms, and has now held three successful licensing rounds for exploration and production rights, securing the participation of major IOCs from around the globe.

The only significant hurdle still standing is the decades-old division of the island, where the internationally recognized ROC controls only the southern two-thirds, while the rest is under the Turkish control through the “Turkish Republic of Northern Cyprus” (“TRNC”). Here too, however, both sides have demonstrated strong commitment to a negotiated reunification, and while the latest round of talks has been delayed by an uptick in tensions, there is still reason to expect a resumption.

Among these reasons is the fact that the new US Secretary of State, Rex Tillerson – whose previous career as head of ExxonMobil makes him singularly well-equipped to understand the importance of Cyprus – has already taken a direct interest in the peace process. We can only hope that the US, the UN, and the EU will exert even more positive pressure to help the talks succeed, including the powerful inducement of having at least some of the region’s gas exports pass through Turkey, which is already one of the world’s most important energy corridors.

TRNC. The governments of Greece and the United Kingdom also have critical parts to play in helping the Cypriot people to achieve reconciliation and start reaping the rewards thereof.

The other question mark in the Eastern Med is my homeland, Lebanon, and while a lot of time has been wasted in the past few years, efforts to gets its house in order are finally back on track.

Until recently, political infighting had blocked Parliament’s election of a new president for more than two years, the Parliament extended its own mandate for nearly three years, and the prime minister and Cabinet were basically caretakers because of widespread perceptions that they lacked legitimacy. Even before this multi-sided impasse, rival political camps were so mutually suspicious that cooperation was impossible.

Despite these headwinds, some crucial preparatory steps were taken. The Lebanese Petroleum Administration was created in 2012, and while political squabbles delayed its work, the LPA still found a way to lay the foundation for the country’s nascent energy sector: all the necessary mechanisms are in place or ready to be rolled out, including tender procedures and draft terms for the fiscal regime.

It is my pleasure to report that other pieces are now falling into place as well. The former commander of the Lebanese Armed Forces, General Michel Aoun, has been elected president, and he enjoys more broadly based support than any of his recent predecessors. He also has made a welcome habit of insisting that Lebanon can only regain its former glory by ensuring and enforcing the rule of law, something that will be essential if the Lebanese are to keep the proceeds of gas exports from being squandered by incompetence or pilfered by malfeasance.

There is a new prime minister too, and he and his Cabinet likewise enjoy relatively strong acceptance. Last but not least, most political factions have gotten serious about holding new parliamentary elections. The usual debate over constituency size and other rules may cause a delay, but most signs point in the right direction.

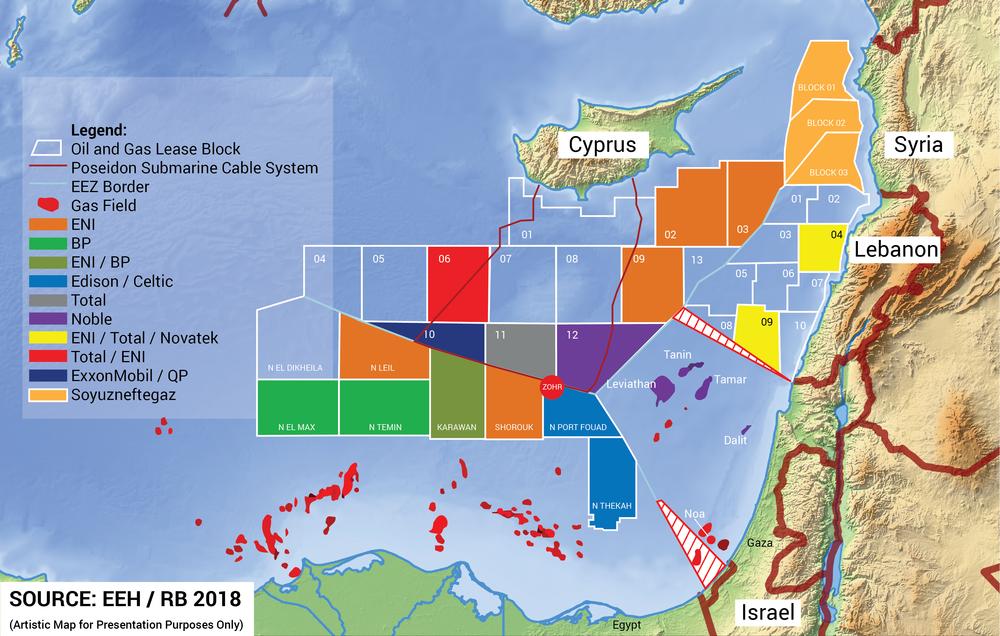

As many had hoped, the LPA has moved quickly to take advantage of improving political conditions. Most tellingly, it has initiated the country’s first licensing round, inviting bids for offshore exploration in five of the 10 blocks it has delineated in Lebanon’s Exclusive Economic Zone (EEZ). At least two of the five blocks are pretty straightforward: Block 4 lies entirely within Lebanon’s EEZ, directly off the coast, while Block 1 lies in the northwest corner, where demarcation has already been agreed with Cyprus. (As far as I know there is no delimitation agreement between Lebanon and Syria. Actually there is a maritime dispute stemming from the tabling by Lebanon of coordinates for its northern EEZ boundary to the UN to which Syria objected in writing).

Blocks 8, 9, and 10 are more complicated because all three are in the south, where Lebanon’s maritime claims overlap with Israel’s. The area in question is less than 5% of Lebanon’s EEZ and an even smaller slice of Israel’s claimed EEZ, which would have been negotiated away under normal circumstances, but the two countries have technically been at war for almost 70 years, punctuated by repeated outbreaks of actual hostilities and even more numerous threats thereof.

The situation is difficult but not impossible. The US and the UN, as well as Cyprus have rendered their good offices in order to find ways to solve the dispute by holding separate talks with Israeli and Lebanese officials, and whatever their other disputes, both sides now have a shared interest in avoiding anything that might hinder energy development. With so much at stake in terms of attracting foreign investment, securing export revenues, and accelerating GDP growth, the cost of another shooting war would simply be too high.

Conversely, the benefits – not just for Lebanon and Israel, but also for their neighbors and their would-be customers – of getting down to business are too attractive to pass up. Reliable supplies of cheap, clean natural gas from the Eastern Med would improve energy security for Turkey, the EU, and other consumer nations. Europe in particular would benefit from lower energy costs, reducing a major burden on households and restoring economic competitiveness. Perhaps most importantly, an East Mediterranean gas boom touched off by diplomacy would set an inspiring example for other regions haunted by longstanding disputes.

Beirut is not out of the woods yet. It still needs to settle several issues, including the establishment of a transparent and accountable Sovereign Wealth Fund to make sure that the benefits of future energy revenues flow to the general population rather than to small groups of economic and political elites. But at least the guiding principles are clear: steer clear of unnecessary frictions with Israel, follow international best practice, and protect the ensuing revenues. Other obstacles may well emerge, but none will be insurmountable if these three rules are followed. REB remarks for Nicosia 2 March 2017

These are truly historic times for the Eastern Mediterranean. The region still has more than its share of problems, but we could be on the verge of a new era – and the energy industry is well-positioned to show the way.

Energy is the lifeblood of modern economies, and all of the science points to massive reserves of oil and (especially) natural gas off the coasts of several Eastern Med countries, including Cyprus, Egypt, Israel, and Lebanon. If responsibly managed, this resource will contribute both directly and indirectly to significant GDP growth, giving these countries the capacity to make long-overdue investments in education, healthcare, infrastructure, transport, and other sectors. In turn, these investments will improve overall competitiveness, raise standards of living, reduce poverty, and set the stage for self-sustaining growth over the long term.

For our region, though, “responsibly managed” means more than just following international business, governance, environmental, and safety standards: it also means finding a way to build and maintain economic and political trust, both between nation-states and within individual societies. Whether we like it or not, we are all partners in this endeavor, so we share an interest in achieving the kind of stability that encourages private investment, reduces trade barriers, and accelerates economic activity across the board. If long-time rivals provide sufficient political and/or diplomatic space for our emerging energy industry to take root, the resulting economic benefits will flow to all concerned, alleviating many of the symptoms – and even some of the causes – of the region’s various problems.

No discussion of this topic is complete without emphasizing the central role to be played by Cyprus. Although every country involved will retain some of its gas production for domestic use, for most of us the real game-changer will be a massive boost in export revenues. There are two ways to get gas to markets in Europe and elsewhere – pipelines and liquid natural gas (LNG) carriers – and Cyprus is clearly the best gateway for both.

Its geographical location, ample coastline, and unique geostrategic position make it: 1) the perfect collection and distribution point for the output of neighbors like Lebanon and Israel; 2) an ideal terminus for one or more pipelines to Turkey and the European mainland; 3) the only viable location for a regional LNG plant; and 4) a natural middleman between regional governments whose relationships are troubled or non-existent. Because of these and other qualities, including its membership in the European Union, Cyprus should be the cornerstone on which the entire edifice of regional energy growth is built.

What is more, the Republic of Cyprus (ROC), has taken serious steps to make the most of these circumstances by establishing a presence at several steps along the region’s energy value chain. It has moved quickly and effectively to make the island an indispensable regional energy hub by passing suitable legislation, setting up a national energy company, and drawing up a world-class regulatory regime. It also has already signed EEZ delimitation agreements with Egypt, Lebanon and Israel, attracted oilfield support, communications, and other service firms, and has now held three successful licensing rounds for exploration and production rights, securing the participation of major IOCs from around the globe.

The only significant hurdle still standing is the decades-old division of the island, where the internationally recognized ROC controls only the southern two-thirds, while the rest is under the Turkish control through the “Turkish Republic of Northern Cyprus” (“TRNC”). Here too, however, both sides have demonstrated strong commitment to a negotiated reunification, and while the latest round of talks has been delayed by an uptick in tensions, there is still reason to expect a resumption.

Among these reasons is the fact that the new US Secretary of State, Rex Tillerson – whose previous career as head of ExxonMobil makes him singularly well-equipped to understand the importance of Cyprus – has already taken a direct interest in the peace process. We can only hope that the US, the UN, and the EU will exert even more positive pressure to help the talks succeed, including the powerful inducement of having at least some of the region’s gas exports pass through Turkey, which is already one of the world’s most important energy corridors.

TRNC. The governments of Greece and the United Kingdom also have critical parts to play in helping the Cypriot people to achieve reconciliation and start reaping the rewards thereof.

The other question mark in the Eastern Med is my homeland, Lebanon, and while a lot of time has been wasted in the past few years, efforts to gets its house in order are finally back on track.

Until recently, political infighting had blocked Parliament’s election of a new president for more than two years, the Parliament extended its own mandate for nearly three years, and the prime minister and Cabinet were basically caretakers because of widespread perceptions that they lacked legitimacy. Even before this multi-sided impasse, rival political camps were so mutually suspicious that cooperation was impossible.

Despite these headwinds, some crucial preparatory steps were taken. The Lebanese Petroleum Administration was created in 2012, and while political squabbles delayed its work, the LPA still found a way to lay the foundation for the country’s nascent energy sector: all the necessary mechanisms are in place or ready to be rolled out, including tender procedures and draft terms for the fiscal regime.

It is my pleasure to report that other pieces are now falling into place as well. The former commander of the Lebanese Armed Forces, General Michel Aoun, has been elected president, and he enjoys more broadly based support than any of his recent predecessors. He also has made a welcome habit of insisting that Lebanon can only regain its former glory by ensuring and enforcing the rule of law, something that will be essential if the Lebanese are to keep the proceeds of gas exports from being squandered by incompetence or pilfered by malfeasance.

There is a new prime minister too, and he and his Cabinet likewise enjoy relatively strong acceptance. Last but not least, most political factions have gotten serious about holding new parliamentary elections. The usual debate over constituency size and other rules may cause a delay, but most signs point in the right direction.

As many had hoped, the LPA has moved quickly to take advantage of improving political conditions. Most tellingly, it has initiated the country’s first licensing round, inviting bids for offshore exploration in five of the 10 blocks it has delineated in Lebanon’s Exclusive Economic Zone (EEZ). At least two of the five blocks are pretty straightforward: Block 4 lies entirely within Lebanon’s EEZ, directly off the coast, while Block 1 lies in the northwest corner, where demarcation has already been agreed with Cyprus. (As far as I know there is no delimitation agreement between Lebanon and Syria. Actually there is a maritime dispute stemming from the tabling by Lebanon of coordinates for its northern EEZ boundary to the UN to which Syria objected in writing).

Blocks 8, 9, and 10 are more complicated because all three are in the south, where Lebanon’s maritime claims overlap with Israel’s. The area in question is less than 5% of Lebanon’s EEZ and an even smaller slice of Israel’s claimed EEZ, which would have been negotiated away under normal circumstances, but the two countries have technically been at war for almost 70 years, punctuated by repeated outbreaks of actual hostilities and even more numerous threats thereof.

The situation is difficult but not impossible. The US and the UN, as well as Cyprus have rendered their good offices in order to find ways to solve the dispute by holding separate talks with Israeli and Lebanese officials, and whatever their other disputes, both sides now have a shared interest in avoiding anything that might hinder energy development. With so much at stake in terms of attracting foreign investment, securing export revenues, and accelerating GDP growth, the cost of another shooting war would simply be too high.

Conversely, the benefits – not just for Lebanon and Israel, but also for their neighbors and their would-be customers – of getting down to business are too attractive to pass up. Reliable supplies of cheap, clean natural gas from the Eastern Med would improve energy security for Turkey, the EU, and other consumer nations. Europe in particular would benefit from lower energy costs, reducing a major burden on households and restoring economic competitiveness. Perhaps most importantly, an East Mediterranean gas boom touched off by diplomacy would set an inspiring example for other regions haunted by longstanding disputes.

Beirut is not out of the woods yet. It still needs to settle several issues, including the establishment of a transparent and accountable Sovereign Wealth Fund to make sure that the benefits of future energy revenues flow to the general population rather than to small groups of economic and political elites. But at least the guiding principles are clear: steer clear of unnecessary frictions with Israel, follow international best practice, and protect the ensuing revenues. Other obstacles may well emerge, but none will be insurmountable if these three rules are followed.