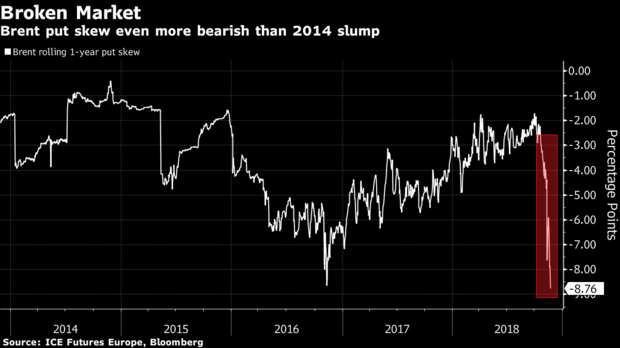

Oil Options Traders Turn More Bearish Than During 2014 Crash

Oil options traders have turned more bearish than when prices plunged back in 2014.

The premiums they’re paying for bearish put options over bullish calls over the next 12 months has reached the largest in data compiled by Bloomberg since 2013. The skew, as it’s known, indicates demand for protection against a slump. The negative bias is far greater than during four years ago, when Saudi Arabia adopted a pump-at-will production policy, helping prices crash to $47 from $115 in a matter of months.

The crude market has been roiled by surging U.S. output and Donald Trump’s unexpected decision to allow buyers of Iranian oil to continue purchases, thereby adding unexpected supply. At the same time the Saudis, under pressure from the American president to help keep prices down, has signaled that it may be producing at a record pace.

Thrown into the mix has been frenetic selling from banks who’ve been forced to sell futures contracts after options contracts that they sold to producers came close to being valuable. The resulting moves have seen crude swing rapidly from talk of $100 a barrel just a few weeks ago, deep into a bear market. Brent traded at about $61 on Friday.

“It shows you the extreme change in perceptions that we’ve just had, the disappointment in expectations,” Thibaut Remoundos, founder of hedging strategies adviser Commodities Trading Corp. in London said of the shift in options markets. “The options volatility market in Brent is broken right now.”

While the premium paid for puts over calls is the biggest in at least five years, it’s not the only corner of the oil options market that has been buffeted by tumbling prices. The CBOE/Nymex Oil Volatility Index, a measure of near-the-money crude options, hit nearly 56 points earlier this week, the highest level in 2 years and almost double where it reached in early November.

The move brings into focus the decisions of some producers to lock in their output when prices were at multi-year highs in recent months.

Remoundos said some producers could have locked in their output for 2019 at $72.50 without any outlay on options contracts, a strategy known as a costless collar. A 128 million barrel hedge by Petroleo Brasileiro SA, as well as Mexico’s national oil hedge — the biggest oil deal of the year — are among those said to have roiled Wall Street banks in recent weeks.

OPEC’s Worst Nightmare: Permian Basin About to Pump a Lot More

The map lays out OPEC’s nightmare in graphic form.

An infestation of dots, thousands of them, represent oil wells in the Permian basin of West Texas and a slice of New Mexico. In less than a decade, U.S. companies have drilled 114,000. Many of them would turn a profit even with crude prices as low as $30 a barrel.

OPEC’s bad dream only deepens next year, when Permian producers expect to iron out distribution snags that will add three pipelines and as much as 2 million barrels of oil a day.

“The Permian will continue to grow and OPEC needs to learn to live with it,’’ said Mike Loya, the top executive in the Americas for Vitol Group, the world’s largest independent oil-trading house.

The U.S. energy surge presents OPEC with one of the biggest challenges of its 60-year history. If Saudi Arabia and its allies cut production when they gather Dec. 6 in Vienna, higher prices would allow shale to steal market share. But because the Saudis need higher crude prices to make money than U.S. producers, OPEC can’t afford to let prices fall.

Cartel Decision

Even so, Saudi Arabia’s output swelled to a record this month, according to industry executives. That means the three biggest producers — the U.S., Russia and Saudi Arabia — are pumping at or near record levels.

A similar scenario unfurled in 2016, when Saudi output rocketed just before OPEC agreed to cuts. This time the cartel’s 15 members, and allies including Russia, Mexico and Kazakhstan, will discuss the possibility of their second retreat from booming American production in three years.

OPEC helped create the monster that haunts its sleep. After it flooded the market in 2014, oil prices crashed, forcing surviving U.S. shale producers to get leaner so they could thrive even with lower oil prices. As prices recovered, so did drilling.

Now growth is speeding up. In Houston, the U.S. oil capital, shale executives are trying out different superlatives to describe what’s coming. “Tsunami,’’ they call it. A “flooding of Biblical proportions’’ and “onslaught of supply’’ are phrases that get tossed around. Take the hyperbolic industry talk with a pinch of salt, but certainly the American oil industry, particularly in the Permian, has raised a buzz loud enough to keep OPEC awake.

Price Tumble

“You’ve got an awful lot of production that can come in very economically,’’ said Patricia Yarrington, Chevron Corp.’s chief financial officer. “If you think back four or five years ago, when we didn’t really understand what shale could do, the marginal barrel was priced much higher than what we think the marginal barrel is priced today.’’

That shift makes shale resilient to a price tumble. After touching a four-year high in October, West Texas Intermediate, the U.S. benchmark, has fallen by more than 20 percent.

Shale Boom

Only a few months ago, the consensus was that the Permian and U.S. oil production more widely was going to hit a plateau this past summer. It would flat-line through the rest of this year and 2019 due to pipeline constraints, only to start growing again — perhaps — in early 2020.

If that had happened, Saudi Arabia would’ve had an easier job, most likely avoiding output cuts next year because production losses in Venezuela and sanctions on Iran would have done the trick.

Instead, August saw the largest annual increase in U.S. oil production in 98 years, according to government data. The American energy industry added, in crude and other oil liquids, nearly 3 million barrels, roughly the equivalent of what Kuwait pumps, than it did in the same month last year. Total output of 15.9 million barrels a day was more than Russia or Saudi Arabia.

Rail Cars

The growth was possible because oil traders decided not to be stymied by the dearth of pipelines. They used rail cars and even trucks to ship barrels out of the region. But pipeline companies unexpectedly increased capacity, in part because they added chemicals known as “drag reduction agents’’ to increase flow. A new pipeline came online earlier than anticipated, and with three more expected between August and December next year, production is poised to soar.

“The narrative has shifted significantly,’’ said John Coleman, a Houston-based oil consultant at Wood Mackenzie Ltd. “Six months ago, the market expected the bottleneck to ease in the first quarter of 2020. Now, it expects it in the second to third quarter of 2019.’’

Knowing that more transportation would be available next year, Permian companies are drilling wells but, for now, aren’t fracking many of them. Those wells are becoming a reservoir of ready-to-tap production once the new pipelines — Gray Oak, Cactus II and Epic — come online.

“We’re going to see a re-acceleration of well completions in the Permian in the second half of 2019,’’ said Corey Prologo, head of oil trading in Houston at commodity merchant Trafigura Group Ltd. “The pipelines are going to fill up very quickly.’’

The only obstacle for another surge is export capacity, as most of the incremental output will need to ship overseas. With terminals nearly full, Permian barrels could end piling up in the ports of Corpus Christi and Houston.

Transportation Bottlenecks

Even so, few in Houston, or in Midland, Texas, the hub of the Permian region, believe that growth will be anything but gangbusters next year because of the clearing of transportation bottlenecks.

“It will be a series of events throughout 2019 that occur,’’ said Jeff Miller, chief executive officer of Halliburton Co., the world’s biggest provider of fracking services. “But it’d be easy to see, as we finish the year, things being perfectly normal.”

American Oil Renaissance

By the end of 2019, total U.S. oil production — including so-called natural gas liquids used in the petrochemical industry — is expected to rise to 17.4 million barrels a day, according to the U.S. Energy Information Administration. At that level, American net imports of petroleum will fall in December 2019 to 320,000 barrels a day, the lowest since 1949, when Harry Truman was in the White House. In the oil-trading community, the expectation is that, perhaps for just a single week, the U.S. will become a net oil exporter, something that hasn’t happened for nearly 75 years.

Saudis Concede

Saudi officials concede that the tsunami is coming. OPEC estimates that to balance the market and avoid an increase in oil inventories, it needs to pump about 31.5 million barrels a day next year, or about 1.4 million barrels a day less than what it did in October.

Global oil demand has so far absorbed the extra U.S. crude barrels, limiting the impact on prices. The loss of output from Venezuela and to a lesser extent, Iran, even allowed Saudi Arabia, Russia and a few others to boost production. But for the cartel, U.S. shale remains as intractable as in the past.

Khalid Al-Falih

Photographer: Simon Dawson/Bloomberg

In early 2017, Khalid Al-Falih, the Saudi oil minister, told an industry forum that Riyadh has learned the lesson that cutting production “in response to structural shifts is largely ineffective.’’ The kingdom would only make one-time supply adjustments to react to “short-term aberrations,” he said, and otherwise allow “the free market to work.”

Nearly two years later, Al-Falih has lost enough proverbial sleep. He’s about to make a U-turn. He’ll battle what increasingly looks like a structural problem: booming U.S. production.

US says economy to be hurt by climate change denied by Trump

The Trump administration just published a major report documenting the advance of climate change, weeks earlier than expected and on a day many Americans are occupied with family and holiday shopping. The news is predictably bad, but this time the tally comes with a price-tag — one significantly larger than you’ll find at the mall. The report catalogues the observed damage and accelerating financial losses projected from a climate now unmoored from a 12,000-year period of relative stability. The result is that much of what humans have built, and many of the things they are building now, are unsuited to the world as it exists. And as time goes on, the added cost of living in that world could total hundreds of billions of dollars — annually. “The assumption that current and future climate conditions will resemble the recent past is no longer valid,” the authors write. President Donald Trump has rejected without evidence the global scientific consensus that humans are doing grave damage to the planet. The Republican has sought to roll back Obama-era ini- tiatives to slow greenhouse gas pollution in favour of fossil fuel interests. In recent years, thousands of Americans have died during, or as a consequence of, extreme weather tied to climate change — from powerful hurricanes fuelled by extremely warm seas to calamitous conflagrations stemming from drought. “The Trump administration can’t bury the eff ects of climate change in a Black Friday news dump — ef- fects their own federal government scientists have uncovered,” said Senator Sheldon Whitehouse, a Democrat from Rhode Island, in a statement. “This report shows how climate change will aff ect every single one of our communities. The president says outrageous things like climate change is a hoax engineered by the Chinese and raking forests will prevent catastrophic wild fires, but serious conse- quences like collapsing coastal housing prices and trillions of dollars in stranded fossil fuel assets await us if we don’t act.” Part of the fourth US National Climate Assessment since 2000 (the last one was in 2014), the report departs from predecessors in that it focuses on money, and how much of it America stands to lose to climate change. The costs assessed range from household expenses to the availability and pricing of food, energy and other goods people use in modern society. And it’s not just the eff ects at home. “The impacts of climate change, variability, and extreme events outside the US are aff ecting and are virtually certain to increasingly aff ect US trade and economy, including import and export prices and businesses with overseas operations and supply chains,” the authors write.

“Now it’s seen much more as a societal or economic issue than a narrow environmental one.” A chapter on how to avoid worst-case scenarios, called mitigation, looks at estimates of economic losses across the economy by sector, pinned to the end of the century. They suggest that policy, technological and behavioural changes that lead to significantly lower emissions can cut potential financial damage across many sectors roughly by half. Nevertheless, such a best case-scenario will still leave Americans in a country where they are paying tens of billions of dollar more annually to ad- dress the fallout of accelerating climate change. A scenario with dramatically less pollution could slash projected losses in 2090 by 48% ($75bn) a year in labour costs, 58% ($80bn) in heat-related deaths and 22% ($25bn) in coastal real estate, according to the report. When the first NCA came out in 2000, researchers were still thinking through how diff erent parts of the US might be vulnerable to natural and human- driven changes. Almost two decades later, the as- sessment incorporates a grim accounting of actual damages, which in turn allows firmer projections of what’s coming. “A lot has happened in 20 years,” said John Furlow, a contributing author and deputy director of Columbia University’s International Research Institute for Climate and Society. “Now it’s seen much more as a societal or economic issue than a narrow environmental one.” Climate change’s impacts, the report states, are presenting painful financial choices for every region of the country: In Pennsylvania, ageing bridges may not fare well against more extreme storms, and wa- ter and wastewater systems need almost $30bn in investment. In general, about 90% of the northeast is built on infrastructure poorly suited to adjust to rising seas.

“Projected future costs are estimated to continue along a steep upward trend relative to what is being experienced today,” the report states. More than 60% of big southeastern cities see heat- wave trends above the national average, and three of them, Birmingham, Alabama, New Orleans and Raleigh, NC, are exceeding the rest of the country across all major heat-wave measures. Anchored by California’s clean-tech economy, the Southwest is seeing much of the nation’s new energy investment. Legacy power technologies, such as water-cooled power plants, will continue to work for decades, however, and will be less eff ective as temperatures make cooling sources too hot. Hot water could reduce eff iciency of these power plants by 15% by 2050. In the Midwest, a major producer of corn and soy- beans, increased temperatures, rainfall and humid- ity have eroded soil and allowed harmful pests and pathogens to thrive, according to the report. Rising growing-season temperatures in the region are pro- jected to be the largest single factor contributing to declines of US agriculture production. A new chapter of the NCA addressing US interests abroad emerged from the previous report’s work on agriculture. The sector directly contributed $136.7bn and 2.6mn jobs to the US economy in 2015. It’s also a significant source of pollution — about 9% of the US total in 2016 — and vulnerable to its impacts both at home and from abroad. “The US food system is a globalised food system, and we import a lot,” said Diana Liverman, a Re- gents’ professor at the University of Arizona. Since the global nature of food-system risk drew interest during the 2014 report discussions, researchers conducted deeper analysis “on things like the vulnerability of US supply chains.” Strange phenomena are playing havoc with the US food supply, including “the loss of synchrony of seasonal phenomena,” the report states, including an emerging disconnect between crops and pol- linators. While scientists are developing climate change resistant crops, the progress has been “modest,” according to the NCA. It calls for more public investment in these projects and notes that — against the claims of some environmental groups — “genetically engineered crops have shown economic benefits for producers, with no substantial evidence of animal or human health or environmental impacts.” The NCA diff ers in important ways from similarly weighty, periodic reports from the UN’s Intergovern- mental Panel on Climate Change. The most recent of these studies explored the diff erence between a world that warms 1.5 degrees Celsius and 2 degrees, the long-time international goal (slower sea-level rise, more Arctic sea ice, some coral left). The NCA authors express concern about growing threats to global trade, supply chains and the price of goods. Other international issues addressed beyond trade include national security, humanitar- ian aid and what the report calls “trans-boundary resources,” such as fish, water and minerals man- aged jointly by neighbouring countries.

Norwegian oil, gas plants shut after tanker, frigate collide (Update)

An oil tanker and a Norwegian navy frigate collided off Norway‘s west coast on Thursday, injuring eight people and triggering the shutdown of a North Sea crude export terminal, Norway‘s largest gas processing plant and several offshore fields.

The frigate, which recently took part in a major Nato military exercise, was tilting on one side and slowly sinking, live television pictures showed. The Norwegian military said it was attempting to save the ship.

“The military is leading a salvage operation in cooperation with the Coast Guards,” Norway‘s armed forces said in a statement.

The Kollsnes gas plant, with a processing capacity of 144.5 million cubic metres per day, has also been shut, Equinor said. It was not immediately clear when it would restart operations.

The plant processes gas from the Troll, Kvitebjoern and Visund fields and sends it to Britain and the rest of Europe. Gas output from the Troll A platform had been shut, said an Equinor spokeswoman.

UK wholesale gas prices were up ahead of the incident and increased further afterwards. Gas for immediate delivery was up 6.2 per cent at 66.50 pence per therm at 1136 GMT. Norway is a major supplier of gas to Britain so big outages can impact UK gas prices.

Flows from Norway to Britain were down by 14-15 million cubic metres due to the outage at Kollsnes.

“Norwegian outages due to the collision have prompted extra buying. The market was already quite bullish due to lower temperatures. It is also not clear how long they (the outages) will last,” a British gas trader said.

There was no sign of any leak from the Sola TS oil tanker, although it would return to port for inspection, rescue leader Ben Vikoeren at the Joint Rescue Coordination Centre for southern Norway told Reuters.

The tanker had left Equinor’s Sture oil shipment terminal with a cargo of crude, and the facility would be temporarily shut as a precautionary measure, the company said.

The Sture terminal receives oil via pipelines from a string of North Sea fields, including the Oseberg, Grane, Svalin, Edvard Grieg and Ivar Aasen, which in turn is exported to global markets on oil tankers.

The Sture terminal has a capacity to store one million cubic metres of crude oil and 60,000 cubic metres of liquefied petroleum gas in rock chambers.

LPG mix and naphtha are also exported from the terminal via the Vestprosess pipeline to the Mongstad oil terminal.

It was not clear for how long the Sture terminal would remain closed, said Equinor, adding that oil output from Oseberg and Grane, which the firm operates, was shut as a result.

Oseberg is one of the crude streams underpinning the global Brent oil benchmark. Brent crude futures were up 71 cents to $72.78 a barrel by 1007 GMT.

Output at Ivar Aasen, which produced about 95,000 barrels of oil equivalents per day in the third quarter, has also been shut down, operator Aker BP told Reuters.

Production at the Edvard Grieg field was also shut down, a source with knowledge of its operations said.

The KNM Helge Ingstad frigate’s crew of 137 had been evacuated, Vikoeren said. Eight people suffered light injuries.

The Sola TS, an Aframax class vessel built in 2017, belongs to Tsakos Energy Navigation, according to the company’s website.

The KNM Helge Ingstad had recently taken part in Nato’s Trident Juncture military exercise, which centred on the defence of Norway.

Russia Looks to Hydrogen as Way to Make Gas Greener for Europe

Russia is looking at how to develop a market for hydrogen in Europe, a move that would help maintain demand for one of its primary exports as governments everywhere work to cut pollution.

Gazprom PJSC, the Russian company that’s the dominant exporter of natural gas into Europe, is exploring ways to produce emissions-free hydrogen from its fuel and create a 153 billion-euro ($175 billion) a year market by 2050, according to a presentation executives from the company made in Brussels last month. That would be bigger than the $110 billion value of Europe’s existing natural gas supply last year.

The effort would bring Russia in step with the government of Japan, oil major Royal Dutch Shell Plc and a handful of companies that are promoting fuel cells and hydrogen as an alternative to electricity generation and transportation fed by fossil fuels. With Europe working to make dramatic reductions in greenhouse gas emissions, Russia is looking for ways to make its gas green enough to remain part of the energy mix. Hydrogen is an option because it can be made from natural gas without generating additional emissions.

“It would not do the entire job but a large part of it,” Michael Faltenbacher, a principal consultant at Germany’s Thinkstep AG, which carried out a study for Gazprom, said at the presentation at Gazprom’s offices in Brussels. “We are looking at a major CO2 reduction potential which will come at a financial cost. There is definitely investments related to that but also opportunities for industry and economy.”

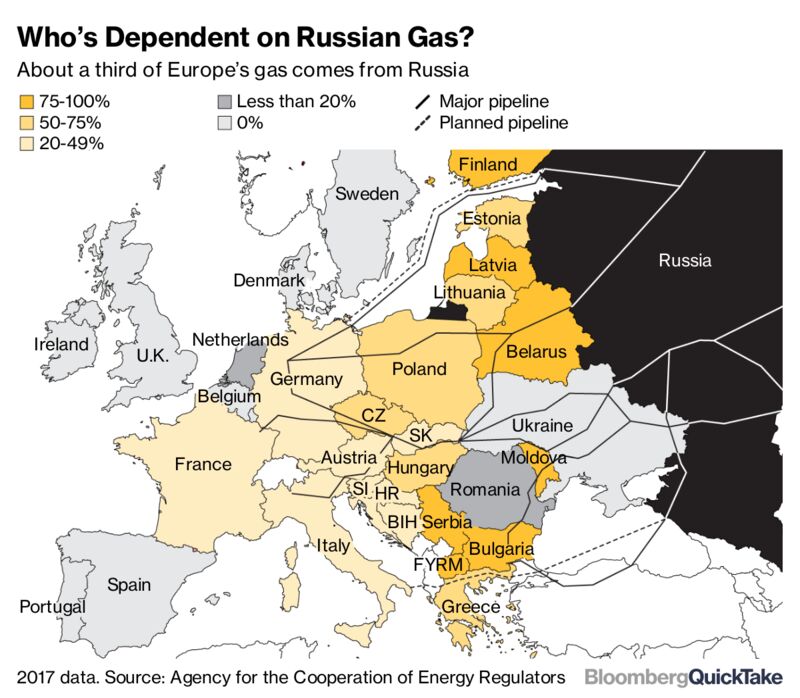

2017 data. Source: Agency for the Cooperation of Energy Regulators

Natural gas already is the main raw material used to make hydrogen commercially, and some of the lighter gas is already blended in a small proportion into Europe’s gas pipeline network. What Gazprom is envisioning is gradually boosting the share of hydrogen in those pipelines and then turning its natural gas into hydrogen through green processes that don’t exacerbate global warming.

While several technologies to produce hydrogen including water electrolysis are being developed, Gazprom is investigating one process known as thermal methane pyrolysis. This reaction takes place in a low-temperature, non-equilibrium plasma that’s put under high pressure in a small reactor. The company is trialing the technology in the Siberian town of Tomsk.

“Natural gas from Russia is now the cleanest available for Europe,’’ Maximilian Kuhn, public affairs expert Gazprom Germany, said at a conference in Berlin on Thursday. “Our proposal is to recognize that natural gas is a solution for Germany to achieve its Paris climate target. We could reach the target based on natural gas.’’

With no contact with oxygen, no CO2 is emitted when hydrogen atoms are split off from natural gas. That process makes a stream of pure hydrogen, with carbon dropping out as a solid instead of escaping into the air as CO2. That solid carbon can be used in industries. If wind or solar farms are used to generate energy needed for that process, zero emissions would be used in manufacturing the hydrogen.

“Gas companies are scared and worried as renewable costs are falling, electricity heating is expanding, and European nations are adopting very strong hydrogen policies, potentially making the entire gas infrastructure redundant,” said Claire Curry, an analyst at Bloomberg NEF in New York. “It sounds interesting if they can capture carbon cheaply, but there are challenges. It is unclear if people will want hydrogen in their homes, and that also wouldn’t help Europe become energy independent.”

Gazprom’s vision is to introduce an emissions-free form of hydrogen into its business over the next few decades. That would help Europe to reduce emissions by 62 percent by 2050, a big chunk of the bloc’s commitment to slash pollution 80 percent by that year from 1990 levels. Gazprom is offering three stages, as outlined below.

From Gas to Hydrogen

Gazprom envisages a 3-stage process to introduce and expand role of hydrogen in its business

NOTE: Total reduction is seen at ~49%. 62% reduction is needed to reach 2050 CO2 target of -80% greenhouse emissions vs 1990. Gap of ~13% seen filled with efficiency measures. Source: Thinkstep

The first stage in the Gazprom program, already being promoted, envisages switching power plants and vehicles to gas from coal and gasoline, respectively. The next stage would involve building up hydrogen in a mix with natural gas.

Current blend limit of hydrogen into gas grids varies from zero in the U.K. to 12 percent in the Netherlands, according to Thinkstep. A mix with as much as 20 percent of hydrogen could be used on the majority of applications, without challenges or infrastructure changes, according to Gazprom.

A ratio of over 25 percent of hydrogen used in the pipeline networks can lead to lower crack resistance in steel pipes and increases over 30 percent may require adaptation of turbines and compressors, according to Thinkstep.

“Pipelines and regulations would have to be changed to allow a higher ratio of hydrogen used in the system,” Bloomberg NEF’s Curry said.

How much hydrogen is allowed in pipelines?

Gazprom is still considering how the business might evolve from there. It may be more viable to produce hydrogen in Europe and then mix it there with gas arriving from Russia, according to Gazprom experts. Any changes would need careful study by Gazprom’s customers, European regulators and other interested groups.

“Natural gas due to its density would make more sense to transport over long distances and then have the hydrogen production locally,” Thinkstep’s Faltenbacher said.

Russia first presented its active contribution to a CO2-free gas provision to Europe during a workshop in Berlin in August, according to a report on the European Commission’s website, which acknowledged the nation’s perspectives of methane cracking, a technology which could provide emissions-free hydrogen at large scale.

This “could be used as a potential and cost efficient transition pathway for introducing renewable based hydrogen in the longer term,” the report said. “Rules for certifying that the carbon by-product from methane cracking is deposited without being released to the atmosphere as CO2 would yet have to be developed.”

The other main process for making hydrogen from natural gas is known as electrolysis, where an electric charge is introduced into a stream of gas to break those molecules into their constituent parts.

The Russian company might be able to make hydrogen at a cost of 1.14 euros per kilogram by 2050, according to Thinkstep. Hydrogen could be produced today in northern Germany via electrolysis, using curtailed wind and the lower end of wholesale power prices, at 2.21 euros per kilogram, a cost that may fall to 1.77 euros by 2025, according to Bloomberg NEF.

Other global energy companies are also looking at hydrogen. Norway’s Equinor ASA has commissioned a feasibility study for a hydrogen plant in July, while Woodside Petroleum Ltd. has held talks with a Japanese hydrogen supply project led by Chiyoda Corp.

Hydrogen is one of the fuels that Shell is providing. Among its initiatives, Shell is part of a joint venture in Germany which is installing a nationwide network of 400 hydrogen fueling pumps. It has also opened hydrogen refueling sites in California, the U.K. and Canada and has announced the construction of 4 more stations in the Netherlands.

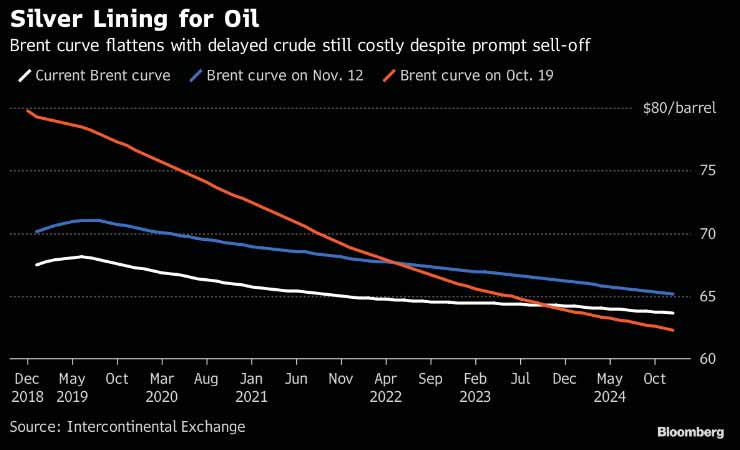

Brent oil curve reveals silver lining as supply woes lurk

For oil bulls who were disheartened by Brent crude’s dire plunge of about 25% over the past few weeks, its forward curve off ers a silver lining, according to Bloomberg. Prices of the global benchmark’s later-dated contracts remain supported due to supply shortage fears.

The curve’s back-end didn’t fall as much as prompt contracts, emerging “relatively unscathed” from the recent sell-off , due largely to years of insuff icient upstream capital expenditures, according to Konstantinos Venetis, a senior economist at TS Lombard.

Oil short-selling jumps in record streak as faith in OPEC wanes

NEW YORK (Bloomberg) — Hedge funds are betting OPEC will struggle to reverse oil’s precipitous plunge.

Their combined wagers against West Texas Intermediate and Brent crude soared for a seventh straight week, the longest global short-selling streak in data going back to 2011. The bearish bets jumped 14% in the week ended Nov. 13 and have tripled since the end of September, according to data from the U.S. Commodity Futures Trade Commission and ICE Futures Europe on Friday.

With oil prices slipping into a bear market, OPEC has promised to do what it takes to cut output. Still, it’s unclear how far the cartel and its allies will go, and it may take a reduction well beyond the 1 MMbpd that’s been publicly discussed to restore faith, said Daniel Ghali, a commodities strategist at TD Securities in Toronto.

“We’ve been through not just a price shock, but a momentum shock,” he said in a telephone interview. “Given that, we don’t think oil will recover these losses in short order without a significant catalyst, and that may have to be OPEC doing more than expected.’

The jump in bearish bets came amid a 12-day losing streak for WTI crude prices, the longest on record, culminating in a 7.1% tumble on Tuesday. Investors received more bearish news on Wednesday as a weekly government report showed a boom in shale drilling pushed U.S. stockpiles up by 10.27 MMbbl, almost three times the median forecast.

The persistent bearishness, after oil had already given back much of its yearly gain, surprised Bill O’Grady, chief market strategist at Confluence Investment Management in St. Louis. Computer driven trades may be adding to the downward pressure, he said, as crude crashes through one technical-support barrier after another.

Still, he and Ghali saw some embers of optimism in an uptick in long WTI bets. “It tells you the bearish news is kind of in the market already,” O’Grady said by telephone. “Perhaps what we ended up getting was traders that looked at this and said, ‘Ok, you’re down 20%, maybe I should start throwing some longs on there.”

Russia wait-and-see stance on Opec+ cuts shows gap with Saudi

Bloomberg/Moscow

Russia’s energy minister insisted the country and its allies in Opec need to watch the oil market in the coming weeks before making any decisions to cut output.

“We need to see how the situation develops in November and early December to better understand both the current conditions and the winter outlook,” Alexander Novak said in Moscow yesterday. His refusal to join Saudi counterpart Khalid al-Falih in calling for a broad production cut shows their different positions persist just weeks before a key Opec+ summit in Vienna.

“We need to make a balanced decision, and so far there are no criteria for it,” Novak said. While producers did discuss potential output curbs at a meeting in Abu Dhabi earlier this month, they agreed to wait until their December summit before making any decision as more clarity on supply and demand is needed, he said.

A week ago, al-Falih said the Organisation of Petroleum Exporting Countries and its allies need to cut about 1mn bpd from October production levels, reversing about half the increase in output they made earlier this year. The Saudi pronouncement came as fears of supply shortages just a few months ago were supplanted by concerns about an emerging glut and collapsing prices.

Since Saudi Arabia and Russia are the two de facto leaders of the Opec+ alliance, their differing stance suggests negotiations on December 7 could prove difficult.

The Saudis need an oil price of $73.30 a barrel next year to balance the fiscal budget, according to the International Monetary Fund. That’s $6 higher than the current price of Brent crude. In Russia, the state budget is much less dependent on oil prices than it was when the country agreed to join Opec-led efforts to rebalance the market back in 2016. President Vladimir Putin said last week that a price around $70 “suits us completely.” Russia’s budget will balance next year even if prices for the country’s export blend drop as low as $40 a barrel, according to the Finance Ministry.

Erdogan, Putin celebrate key step in Russia-Turkey gas pipeline

AFP Istanbul

Turkish President Recep Tayyip Erdogan and Russian counterpart Vladimir Putin on Monday marked the completion of the offshore phase of a gas pipeline underneath the Black Sea, the latest sign of burgeoning co-operation between Ankara and Moscow.

Erdogan hailed the TurkStream pipeline, which aims to pump some 31.1bn cu m of gas from Russia to Turkey annually, as a “new step” in Turkish-Russian energy cooperation, which he said showed the “high level” of relations between the two countries.

Yesterday’s ceremony marked the completion of the building of two undersea lines stretching 930km (578 miles) across the Black Sea from Anapa in Russia to Kiyikoy in Turkey at a depth of some 2km (6,500ft).

The pipeline was laid by the special pipe-laying vessel Pioneering Spirit, which is the area of some six football pitches.

Putin and Erdogan watched via video link in Istanbul as the last section was welded and laid into the sea by the vessel.

Putin said he believed TurkStream and the Akkuyu nuclear power station would become “clear symbols of the growing development of Russia and Turkey’s multi-faceted partnership.”

“This (TurkStream) will without doubt turn Turkey into a serious European hub and this will without doubt have an effect on the geopolitical position of the Turkish Republic,” he added.

The onshore section of the pipeline in Turkey still needs to be built and TurkStream expects the gas to start being pumped at the end of 2019.

The aim is that half of the gas pumped through the pipeline will go to ensure the energy needs of western Turkish cities like Istanbul, Bursa and Izmir and the other half sent on to other European countries.

Despite in theory being on opposite sides of the Syrian civil war, regime backer Russia and rebel supporter Turkey have worked closely to end the conflict and stave off a government assault to re-take the key region of Idlib.

Meanwhile, Ankara and Moscow have agreed terms on the delivery of S-400 missiles in a deal that had alarmed Nato member Turkey’s Western allies.

“We have never determined our bilateral relations with Russia according to demands or pressure from other countries,” Erdogan said to loud applause.

Putin meanwhile personally praised Erdogan, saying the TurkStream project could not have been released without the Turkish president.

“Such a project needs political will and courage. Because in the circumstances of growing competition such projects cannot be without this,” he said.

Both leaders also reaffirmed their goal to lift annual bilateral trade volumes to $100bn, which Putin said was the same as between Russia and China.

“Why should it be less with Turkey? We will achieve this result. I don’t even doubt this,” said Putin.

Norway lawmakers call for scrutiny of wealth fund Saudi holdings

Norwegian socialist lawmak- ers are stepping up pressure to review the country’s $1tn wealth fund’s investments in Saudi Arabia after the killing of journalist Jamal Khashoggi. In a proposal to parliament put forward last week, lawmakers rep- resenting the small Socialist Left Party demanded an overhaul of the country’s ties with Saudi Arabia, including the wealth fund’s hold- ings in the kingdom. Legislators, including the party’s standing member on the Finance Committee, Kari Elisabeth Kaski, said the government needs to ex- amine whether the investments are in compliance with the fund’s ethi- cal and human rights framework. They also asked for a review of all investments in weapon producers and the supply of weapons to the war in Yemen. It’s unclear if the motion will receive broader backing from the main opposition party, Labor, or the three-party minority govern- ment. Abid Raja, a key lawmaker for the Liberals, a member of the ruling coalition, also last month called on the fund to divest from Saudi Arabia. At the end of last year, the fund held about $831mns in Saudi Arabian stocks, invested in 42 companies. The holdings have more than doubled since it entered Saudi Arabia in 2015, but records show that it dumped its holding in Saudi Telecom Company. The fund was set to increase its investments in Saudi Arabia due to the country being included in in- dexes, but that was put on hold by the government earlier this month amid a broader global review. Also earlier this month, Nor- way’s Foreign Minister Ine Eriksen Soreide said that the government will halt any new export licences for sales of defence material to Saudi Arabia.