Thirst for oil threatens a pristine Arctic refuge

Trump administration is hurriedly clearing way for exploration It is the last great stretch of nothingness in the United States, a vast landscape of mosses, sedges and shrubs that is home to migrating caribou and the winter dens of polar bears. But the Arctic National Wildlife Refuge — a federally protected place of austere beauty that during a recent flyover was painted white by heavy snowfall — is on the cusp of major change. The biggest untapped onshore trove of oil in North America is believed to lie beneath the refuge’s coastal plain along the Beaufort Sea. For more than a generation, opposition to drilling has left the refuge largely unscathed, but now the Trump administration, working with Republicans in Congress and an influential and wealthy Alaska Native corporation, is clearing the way for oil exploration along the coast.

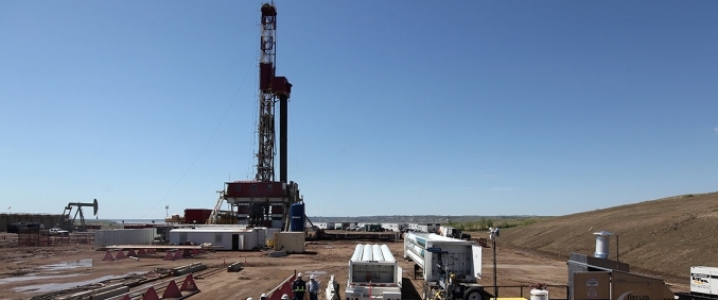

Decades of protections are unwinding with extraordinary speed as Republicans move to lock in drilling opportunities before the 2020 presidential election, according to interviews with over three dozen people and a review of internal government deliberations and federal documents. To that end, the Trump administration is on pace to finish an environmental impact assessment in half the usual time. An even shorter evaluation of the consequences of seismic testing is nearing completion. Within months, trucks weighing up to 90,000 pounds could be conducting the tests across the tundra as they try to pinpoint oil reserves. The fate of the refuge’s coastal plain is in the hands of Ryan Zinke, the interior secretary, who has appointed top deputies with deep professional and political ties to Alaska to oversee its development. Congressional approval to open the area to oil exploration was inserted in tax overhaul legislation last December under the guise of generating revenue for the federal government, and by next year, the Interior Department expects to begin selling the first drilling leases.

The hurried timeline has created friction, with some specialists in the federal government concerned that environmental risks are being played down or ignored. And many outside scientists and environmentalists share the concerns, warning that plans for seismic testing and eventual drilling could harass, injure or kill polar bears and other wildlife. “It seems as though the administration is in a headlong rush to put the drill bit into the coastal plain,” said David J. Hayes, a deputy interior secretary in the Obama and Clinton administrations. “Given the virgin territory of the refuge, with the unique wildlife dependency issues, I don’t know how you do this in an artificially fast and truncated fashion.” Mr. Zinke’s Alaska-friendly appointees, who have long pushed for oil exploration in the coastal plain, say the fears are overstated. They point out that years ago, Congress left open the eventual possibility of allowing development there. Exploration is in the best interest of Alaskans, they say. “I feel like there is a lot of expectations, hopes and dreams from people who I know and love that are riding on this,” said Joe Balash, one of the appointees, who has worked in Alaskan political circles for two decades and now oversees the Bureau of Land Management.

An Alaska Native company, Arctic Slope Regional Corp., has been a major force behind the push and stands to enjoy a windfall if drilling proceeds. The corporation, which has been awarded more than $7.5 billion in federal contracts in the past 10 years, expanded its lobbying under the Trump administration, records show, and Mr. Zinke appointed one of its executives to a top post. Known as A.S.R.C., it is among 13 regional businesses created in the 1970s to foster economic development among Alaska’s indigenous population. It has myriad financial interests in the state’s oil-rich North Slope region, which includes the refuge’s coastal plain and Prudhoe Bay, home to one of the largest oil fields in North America. And it has been a key financial backer of Senator Lisa Murkowski, Republican of Alaska, who has been the drilling plan’s biggest champion in Congress. Many Natives on the North Slope — including Inupiat who live in Kaktovik, the village inside the refuge — support oil development.

But a different Native group that lives south of the refuge, the Gwich’in, fears oil development would disturb the migration of porcupine caribou, animals it has hunted for centuries and still relies on for much of its food. Ms. Murkowski declined to comment, as did Alaska’s other elected representatives in Washington. Mr. Zinke also declined to comment. But he told a Senate committee in March that he was “very bullish on the Arctic.” A HISTORY OF FRUSTRATION The struggle over oil exploration in the Arctic National Wildlife Refuge has its roots 50 years ago in the discovery of petroleum reserves around Prudhoe Bay, west of the refuge. In 1980, when Congress voted to conserve much of the federal land in Alaska, drilling advocates pushed for oil and gas development on the coastal plain. Then, as now, the move was supported by many Alaskans, who generally favor oil development, in part because some of the revenue is returned to them in the form of an annual dividend. The advocates were unsuccessful but had an opening: The 1980 bill allowed Congress to authorize oil and gas development at a later date. The 1.5-million-acre coastal plain, identified in Section 1002 of the legislation, has been known since as the 1002 Area. Despite the close ties, industry officials insist they are not getting a free pass.

“I’m not expecting a rubber stamp,” said Kara Moriarty, the chief executive of the Alaska Oil and Gas Association, who has a framed photo with Mr. Zinke in her Anchorage office. “I’m expecting a very diligent and thorough process.” But those who oppose drilling in the refuge, including many Democrats in Washington, suspect the Department of Interior is not being so diligent. Representative Raúl M. Grijalva, Democrat of Arizona, who will become chairman of the House Natural Resources Committee next month, said he would probably call a hearing about the Arctic development with the goal of slowing it down. “We can make sure that corners are not being cut,” said Mr. Grijalva, who last week called for Mr. Zinke to resign because of ethics allegations against him, prompting a personal attack from the secretary. Scores of environmental organizations are also watching closely, ready to sue whenever an opportunity arises. “There’s going to be damage, going to be long-lasting effects from what they do,” said Geoffrey L. Haskett, president of the National Wildlife Refuge Association and a former Alaska regional director with the United States Fish and Wildlife Service, the managing agency of the refuge. “I just can’t imagine that what we’re going to see is going to be adequate,” he added, referring to the environmental evaluations.

The decision to conduct an environmental assessment of the seismic testing proposal, a less rigorous review than a full environmental impact statement, was especially troubling for many drilling opponents. They point to damage done to the tundra by seismic testing in the mid-1980s; some vehicle tracks from that work remain visible more than 30 years later. And they worry about the disruption of polar bears. Steven C. Amstrup, chief scientist with Polar Bears International, a conservation group, said the coastal plain in the refuge “is the most important maternal denning area” for the southern Beaufort Sea population. Dr. Amstrup, a former United States Geological Survey zoologist who has studied the bears for three decades, said his research had shown that the heat sensing technology used to detect dens would probably miss about half the dens, which would probably be disturbed during the seismic work. Jeff Hastings, chairman of SAExploration, part of the seismic-testing joint venture, said improved technology would prevent damage to the tundra this time around. He also said his company was working with the Interior Department on ways to protect the bears. CORPORATE MUSCLE When Mr. Zinke went in search of influential Alaskans to fill top posts in his Interior Department, he turned to people who had worked for elected officials in the state and for past Republican administrations in Washington. He also looked to A.S.R.C., a multibillion-dollar business that stands to gain the most financially if drilling commences in the 1002 Area.

Tara Sweeney, its former executive vice president for external affairs, is now assistant secretary for Indian affairs. With nearly $2.7 billion in annual revenue, A.S.R.C. is the largest of the Alaska Native corporations and ranks 169th on Forbes’ nationwide list of private companies by revenue. Still, A.S.R.C. has little name recognition outside Alaska, allowing it to attract relatively little attention while lobbying. But there are deep disagreements over A.S.R.C.’s role in the drilling campaign, and whether its corporate interests align with those of Native families who have lived off the land for generations. For decades, the Gwich’in have led the Native opposition to drilling, arguing that opening the 1002 Area could affect the porcupine caribou, a major source of food and a spiritual touchstone. “We are asking to continue to live the way we always have,” said Bernadette Demientieff, the executive director of the Gwich’in Steering Committee, which opposes oil development in the refuge and recently joined with the Sierra Club to try to persuade banks to hold back financing for exploration. Matthew Rexford, the tribal administrator of Kaktovik and the president of Kaktovik Inupiat Group, said the drilling could be done responsibly and should go forward. Unlike the Gwich’in, Rexford’s village stands to benefit financially. “I have given this a lot of thought, and our community has given this a lot of thought,” he said. “We do feel it can be done in an environmentally safe and sound manner.”