ثروة “كاريش” بين 22 و25 مليار دولار

كَثُرَت في الفترة الأخيرة الخيارات المتاحة في نظر بعض المسؤولين في لبنان، لتأمين مصادر يتم عبرها تسديد أموال المودِعين… فما أن طُرِح إنشاء الصندوق السيادي، حتى ارتأى البعض اللجوء إلى رهن جزء من احتياطي الذهب… لكن ما لم يكن في الحسبان أن يقترح أحدهم استخدام أموال ثروة لبنان النفطية لتسديد الودائع ولتغطية كلفة الدين العام! علماً أن مفاوضات ترسيم الحدود البحرية بين لبنان وإسرائيل عالقة منذ أيار 2021، ولا تزال الضبابية تلف هذا الملف محلياً ودولياً.

الخبير الدولي في مجال الطاقة رودي بارودي يعلّق, في حديث إلى موقع القوات اللبنانية الإلكتروني، على الفائدة المالية من حقول النفط التي يؤمَل أن تشكّل الثروة النفطية للبنان، ليؤكد أنه “في حال حصول لبنان على جزء من حقل كاريش, فإن حصته لا تكفي لتغطية الدين العام اللبناني حتى وفق أسعار النفط والغاز المعتمدة حالياً”، ويقول “ربما قد تغطي حصّة لبنان من حقل كاريش أو غيره، جزءاً ضئيلاً فقط من الدين العام”.

ويعتبر أنه “من غير المؤكد ما إذا كان لبنان سيتمكّن من الحصول على الخط 23، من دون معالجة مجموعة من الأخطاء الجسيمة التي ارتُكِبَت عند البدء بوضع الخطوط من 1 الى 23 قبل نحو 12 عاماً”.

ويكشف بارودي عن أن حقل “كاريش” المكتشَف العام 2013 يحتوي على 2.5 ترليون قدم مربّع من الغاز. وهذا الحقل تم اكتشافه من قبل الشركة الإسرائيلية “ديليك” العام 2013 والتي باعته بدورها إلى “إينيرجيان”.

ويقول، إذا تم احتساب الكمية على أساس أسعار الغاز والنفط الحالية، فإن المردود المتوقع من حقل “كاريش” يتراوح ما بين 22 و25 مليار دولار أميركي. لكن لا يمكن تقدير مردود حقل “قانا” لأنه قد يكون ممتداً إلى إسرائيل، كما أن حقل “كاريش” متداخل بين لبنان وإسرائيل.

ويُلفت إلى أن إسرائيل أنجزت التحضيرات اللازمة لبدء الإنتاج النفطي وذلك بعد أعوام عدة من الدراسات وعمليات الاستكشاف، فقد عاودت شركة “إينيرجيان” المطوِّرة لحقل “كاريش” الحَفر في الحقل ذاته بحثاً عن المزيد من الغاز والنفط، ويوضح أن “إسرائيل تقوم حالياً بالحَفر في محاذاة الخطّ اللبناني التفاوضي “29” لتنتقل بعد ذلك إلى شمال “كاريش”.

ويُذكِّر في السياق بأن “لبنان أعلن في رسالَتَيه إلى الأمم المتّحدة الأولى في 22 أيلول 2021 والثانية في 28 كانون الثاني 2022، أن حقل كاريش يقع في منطقة متنازع عليها… لكن على الرغم من ذلك، يتم التنقيب في المياه المتنازَع عليها عموماً، ولا سيما في البلوك رقم “9” المُعطّل حالياً إلى أن تُحّل قضية الترسيم بين لبنان وإسرائيل”.

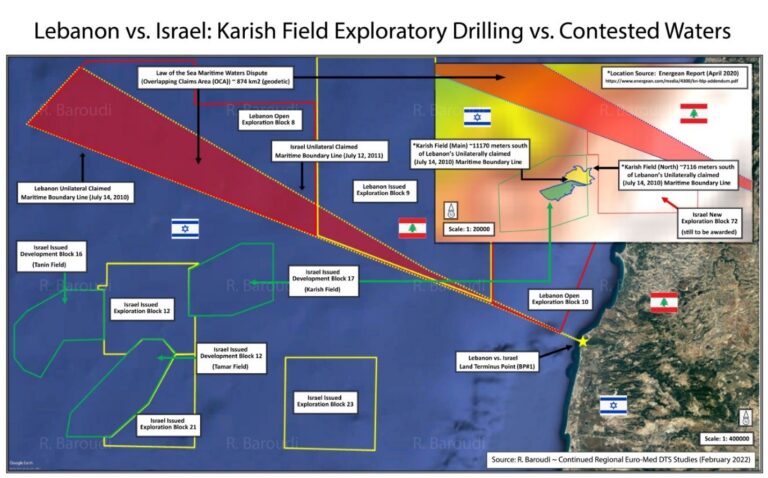

أما بالنسبة إلى الموقع الجغرافي لحقل “كاريش” المكوَّن من جزءين: شمالي وجنوبي (الخريطة مرفقة)، يؤكد بارودي من خلال الدراسة التي أعدّها خلال السنوات الممتدة من العام 2011 إلى العام 2021، أن “حقل كاريش الشمالي يَبعد عن الخط المقترح من قبل لبنان في 14 تموز 2010 (الخط 23) حوالي 7 كلم و116 متراً، كما أن حقل كاريش الجنوبي يَبعد عن الخط نفسه، حوالي 11 كلم و170 متراً جنوباً، وذلك بحسب الخريطة المرفقة والتي تؤكد المواقع والبُعد عن الحَقلين”.

أما بالنسبة إلى البلوك الإسرائيلي الرقم “72” والمتداخل في الأراضي اللبنانية، فهو ملاصق بشكل مباشر للخط “23”، بحسب بارودي.