LNG Canada CEO sees no scenario that would stop its project

Bloomberg/Vancouver

The head of LNG Canada said he does “not see a single scenario” that would stop the nation’s largest infrastructure project from getting built, dispelling concerns that the $30bn gas export facility is at risk of mounting opposition from pipeline foes.

The liquefied natural gas project in northern British Columbia was approved by Royal Dutch Shell Plc and four Asian partners in October after obtaining the support of the province and 20 First Nation groups. But it continues to face a legal challenge disputing the constitutionality of the project’s approval, as well as protests by a group of indigenous holdouts.

“I do not see a single scenario that would cause the construction of this pipeline to be stopped,” Andy Calitz, LNG Canada’s chief executive officer, said in an interview in Vancouver.

TransCanada Corp is planning to build the pipeline that will carry the gas from western Canada’s prolific Montney shale formation to the coastal export facility in Kitimat. The whole project – including the gas fields, pipeline and liquefaction terminal – fall within British Columbia and was authorised by the provincial regulator.

But a private citizen in Smithers, Michael Sawyer, mounted a legal challenge saying the pipeline is a federal undertaking and should have sought approval from the National Energy Board. The federal regulator agreed in December to consider the jurisdictional challenge and has requested evidence from the parties involved with final oral arguments set for March.

“It’s a complex world – the paths are not clear,” Calitz said. Any decision by the federal regulator could later be appealed in the courts. “But what I am clear about is that this pipeline, by the time that happens, will be in advanced construction.”

Separately, TransCanada is seeking to sell a stake in the pipeline project. That move was long contemplated and doesn’t indicate that there are growing concerns about the project’s risks, Calitz said.

“It has always been a part of the financing strategy for the project,” Calitz said. “It has no impact on either the construction or the capacity or any other aspect of the project.

Russia eyes greater energy dominance as Novatek taps Arctic

Bloomberg Moscow/London

Almost 1,500 miles from Moscow, the tiny port of Sabetta nestles in a desolate Russian Arctic peninsula. A former outpost for Soviet geologists, it’s now the site of Russia’s most ambitious liquefied natural gas project, operated by a company that only entered the market just over a year ago.

Several times a week, a giant tanker leaves this remote place carrying the super-chilled fuel to buyers in Europe and Asia. It’s not the only LNG plant beyond the Arctic Circle, but it’s by far the largest.

Novatek PJSC, the main shareholder of the Yamal LNG plant, says plans for further projects will transform Russia into one of the biggest exporters of the fuel within a decade. Already the world’s top exporter of pipeline gas and second-biggest shipper of crude oil, exports from Sabetta are giving Russia another conduit into the world economy for the country’s unrivalled energy resources.

“Russia can be in the top four main LNG exporters,” Novatek’s chief financial officer Mark Gyetvay said in an interview in London.

Novatek has demonstrated that it’s possible to produce and liquefy the fuel in such harsh conditions at competitive prices and ship it to markets thousands of miles away in Europe and Asia. That’s helped by receding Arctic ice which is allowing a specially built fleet of strengthened tankers to ship fuel along Russia’s northern coast.

President Vladimir Putin has been a long-standing supporter of developing oil and gas resources locked under the region’s permafrost. When opening the first production train of the Yamal LNG project in late 2017, Putin said the region gives Russia the opportunity to take up the fuel’s “niche it deserves.”

“We can boldly say that in this century and the next, Russia will expand thanks to the Arctic,” he said at that time.

Novatek, whose biggest shareholders include Russian billionaires Leonid Mikhelson and Gennady Timchenko, as well as French energy giant Total SA, became Russia’s top LNG producer after starting up its plant in the Yamal peninsula almost two years ago. The facility reached its full capacity at the end of 2018, ahead of schedule, doubling Russia’s share of the global LNG market to 8%.

The gas producer has aggressive plans to command a 10th of the global market by 2030, Gyetvay said, and position Russia as one of the world’s largest exporters alongside the US, Qatar and Australia.

All three of Yamal LNG’s production units, with a combined actual capacity of 17.5mn tonnes a year, are now online. Novatek is attracting partners for a second plant, the so-called Arctic LNG 2 project, which is expected to come online in 2022.

The company is also considering commissioning a third facility and may increase its LNG production target for 2030 by about 20%, to as much as 70mn tonnes a year.

Novatek’s resource base at two Arctic peninsulas – Yamal and Gydan – allows the company to raise production volumes to as much as 140mn tonnes a year in future, according to its chief executive officer Mikhelson.

Russia, the world’s largest gas exporter, has been slow to join the global LNG boom as it has focused investment on pipeline supplies to Europe. Until recently, the country had just one liquefaction project in operation, the Gazprom PJSC-led Sakhalin 2 project near Japan with an annual capacity of about 10mn tonnes.

The country has now taken an interest in the market for tanker-borne fuel amid growing global LNG demand and more difficult relations with its customers in the European Union.

Russia’s Energy Ministry pegs total gas in place within the region at about 210tn cubic meters, or over 70% of the nation’s total. Novatek’s Arctic gas reserves are “conservatively” estimated at about 3.3tn cubic meters, Gyetvay said.

“We believe that Russia could be the fourth or even the third” biggest holder of LNG production capacity, said Karen Kostanian, Moscow-based oil and gas analyst for Bank of America Merrill Lynch.

Putin Keeps Options Open on Possible Extension of OPEC+ Oil Cuts

President Vladimir Putin kept his options open on whether to extend Russia’s joint oil-production cuts with OPEC beyond June, saying he wanted to continue cooperation with the group but also highlighting the many uncertainties in the market.

Russia is comfortable with current oil prices, which rose to a four-month high above $70 a barrel in London on Monday, Putin said at the International Arctic Forum in St. Petersburg on Tuesday. The president also said he doesn’t support an “uncontrollable” increase in the cost of crude that could hurt his country’s other industries.

“We’ll coordinate with OPEC and take a decision depending on the market situation,” at the next meeting in June, Putin said.

Russia, one of the architects of the deal between the Organization of Petroleum Exporting Countries and its partners, has taken a wait-and-see approach on whether to extend the cuts. The political situation in Venezuela, Libya and Iran will need to be considered before a decision is taken, Putin said. Saudi Arabia, which has cut output more than agreed, doesn’t plan to deepen its curbs as the markets are “healthy.”

“Of course, we are closely monitoring the market together with our partners, first of all, with the main oil producers, Saudi Arabia and countries of the Persian Gulf,” Putin said.

Venezuela, Iran

U.S. sanctions have eliminated a significant volume of oil exports from Venezuela and Iran, helping drive up the price of international benchmark Brent crude by more than 30 percent this year. Meanwhile, Libya’s output has been frequently disrupted as armed factions battle for political supremacy.

The Russian president also highlighted the possibility that any of those countries could become a bearish influence on prices. If the U.S. were to seize Venezuelan crude and sell it on the global market, or decide to loosen sanctions on Iran to foster a political compromise, inventories could start to increase again, Putin said. The situation in Libya could also normalize, allowing the country to boost exports, he said.

Russia will also take into account its domestic oil companies’ plans while deciding on the future of the OPEC+ deal, Putin said.

“We understand that output shouldn’t stop, investment should come into the sector, otherwise that also may create problems both for us and global energy,” Putin said.

Big Oil haunted by cost risks as $144bn LNG tab looms

Bloomberg/ Singapore

The world’s biggest energy companies are finally ready to invest in new gas export projects. Now they just need to figure out who will build them, and for how much.

After four years of belt-tightening, oil and gas firms are expected to start spending again, with as much as $144bn of investments in new liquefied natural gas developments in line to be approved by the end of this year. Meanwhile, the engineering, procurement and construction sector that erects these projects has been weakened by the cost-cutting, with shrinking order books and solvency questions.

While the order binge could provide a lifeline to EPC companies, it may see too many projects chasing too few builders, increasing risks for energy firms seeking to keep costs under control. In the last LNG building boom, for instance, projects in Australia alone went over budget by a combined $40bn.

“We have a new wave of LNG projects coming and a decimated construction sector,” said Saul Kavonic, an energy analyst at Credit Suisse Group AG. “There’s real risk as we go into this next wave that engineering and construction constraints mean a return of project delays and cost inflation.”

Natural gas is core to future growth for energy giants, with consumption seen growing faster than oil and coal as policies shift toward lower carbon emissions. Royal Dutch Shell Plc and Exxon Mobil Corp have in the past six months sanctioned new LNG plants in Canada and Texas, the first final investment decisions since 2015 for onshore greenfield projects. The amount of new production capacity investments this year could set a record, according to Wood Mackenzie Ltd.

That’s welcome news to oil and gas EPC companies, which have seen their order books dry up since the oil price crash in 2014. Six of the top publicly traded firms had a combined backlog of more than $120bn in 2014. That fell to about $66bn last year, according to filings from the companies, which now number five after an acquisition.

“The market has gone through a shake-up,” said Peter Coleman, chief executive officer of Australia’s Woodside Petroleum Ltd, which is planning an expansion at its Pluto LNG project. “Some people are still in balance sheet repair, and it hasn’t finished yet. We are watching that very closely.”

The sharpest pain is being felt by Chiyoda Corp and McDermott International Inc, which have suffered from cost overruns related to their work on the Cameron LNG project in Louisiana. Chiyoda in February requested financial aid from Mitsubishi Corp, its largest shareholder, and the company plans to be more selective when choosing future LNG projects and joint venture partners, Tomoyuki Tsukamoto, head of investor relations at Chiyoda, said by phone. McDermott declined to comment.

“We have to recognise that our workforce and our capacity are limited,” Tsukamoto said. “We have to select the most appropriate projects for us.”

A weaker construction sector will be good for the remaining EPC companies, as they’ll have more leverage when it comes to negotiating, said Kavonic. That will mark a reversal from the past few years, when spending cutbacks forced service and construction firms to slash margins and take on more risk to win a limited number of jobs.

While construction companies have worked to lower costs for customers, some energy firms anticipated those numbers would keep dropping, Bechtel Group Inc LNG General Manager Darren Mort said in a phone interview. As projects get closer to final investment decisions, companies are reining in those expectations for more appropriate pricing levels, he said.

“Some of the aggressive numbers don’t seem to be getting the traction that they thought they would,” Mort said. “If they really had some reality to them, we’d be seeing FIDs on that basis.”

San Francisco-based Bechtel is privately held, so its financial data aren’t as accessible as some competitors. The firm has avoided any recent high-profile construction problems and Mort said its finances and capabilities remain strong.

The earlier a company is able to start construction, the less chance that firms push for higher rates, Credit Suisse’s Kavonic said. Shell’s decision to go ahead with LNG Canada in October means the project, which will be built by Fluor Corp and JGC Corp, could be more competitive globally by missing any cost inflation, he said.“The faster projects FID, the better rates they’ll get from the EPC contractors,” said Fauziah Marzuki, an analyst with BloombergNEF in Singapore. “Once the contractors realise they’ll be a bit stretched, they’ll start to factor in bigger contingency costs and margins.

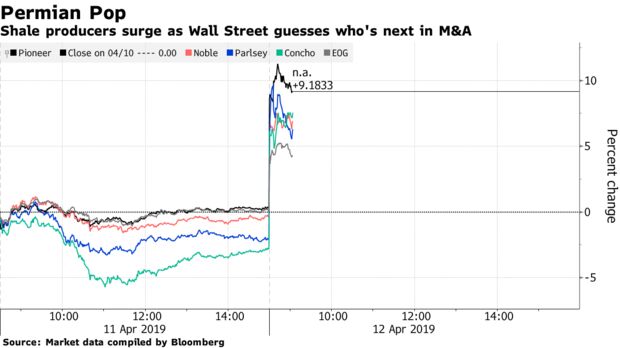

Chevron’s Anadarko Bid Seen Heralding Permian Shale Deals

Chevron Corp.’s $33 billion bid for Anadarko Petroleum Corp. may presage a new Permian Basin buying spree, with Pioneer Natural Resources Co. and Concho Resources Inc. among the next prime targets.

Pioneer, Concho and Noble Energy Inc. surged Friday after Chevron unveiled plans to buy Anadarko, a deal that expands the supermajor’s presence in the Permian region, Gulf of Mexico and East Africa. The transaction vaults Chevron into the rarefied air of rivals Exxon Mobil Corp. and Royal Dutch Shell Plc, which in turn may be roused to make acquisitions of their own.

“Best day in years,” said Todd Heltman, senior energy analyst at Neuberger Berman Group LLC, which has $323 billion under management. “The space really needs consolidation. Maybe the time is finally right given the outperformance of the majors.”

Occidental Petroleum Corp., fresh off its own failed bid for Anadarko, may now find the tables have turned as its hefty footprint in the world’s biggest oil field attracts the attention of acquisitive rivals. Investment bank Tudor Pickering Holt & Co and BP Capital Fund Advisors LLC both cited Occidental as a potential target.

“Everyone is trying to figure out who’s next,” Heltman said.

“From a big-picture perspective, the majors have really bought into shale, but from an asset perspective, the majors don’t necessarily have the right asset portfolios,” Tudor Pickering’s Matthew Portillo said by telephone. “We do think this is going to be the spark that really catalyzes a lot of M&A.”

For Exxon, buying Pioneer or Concho would help the oil giant plug a hole in its Permian portfolio, Portillo said. Shell also will feel pressure to buy more acreage in the prolific stretch of West Texas and New Mexico, possibly by acquiring smaller players like WPX Energy Inc. and Cimarex Energy Co., Portillo said. BP Plc may too embark on expansionist takeovers, he added.

Buying Neighbors

The peculiar nature of shale exploration is an impetus for acquisitions. Unlike in conventional oil fields, shale requires sideways drilling to access crude-soaked rocks, so the further a company can drill horizontally, the more oil it captures. In that context, buying neighboring drillers makes a lot of sense.

For Chevron, Anadarko presented an enticing target. In addition to vast deepwater holdings in the Gulf of Mexico and an ambitious liquefied gas development in Mozambique, the company controls Permian drilling rights across an area twice the size of Los Angeles. Multiple layers of oil-rich shale extend for more than 1.5 miles (2.4 kilometers) underground within that zone.

The most obvious target companies “are the ones that represent the same opportunity Anadarko presented to Chevron,” said Ben Cook, a portfolio manager at BP Capital in Dallas. “It becomes a game of matching up maps.”

What Bloomberg Intelligence Says

“Anadarko was an acquisition target during a weaker price environment for the industry, so we’re puzzled why it agreed to Chevron’s offer when fundamentals are improving. The valuation is disappointing and we think other reasons are behind the deal. Expect Anadarko shareholders to resist the price despite passive-fund representation.”

— Vincent G. Piazza and Evan Lee, analysts

Click here to view the piece

In addition to Pioneer and Concho, Cook highlighted EOG Resources Inc., Occidental and Parsley Energy Inc. as names that could fit the bill for supermajors on the prowl. Noble was also floated as a top-three candidate in a note by RBC Capital Markets.

“You see a deal like this and it does tend to kick off a wave of M&A activity,” Cook said. “This is yet another confirmation that shale development and the short-cycle barrel is increasingly attractive to the majors.”

High Overhead

Investors have pressured producers to cut administrative costs or consolidate

Note: Chart shows expected 2019 general & administrative costs as a percentage of EBITDA esimates

Investors have been pressing shale producers to consolidate in order to gut overhead costs and increase shareholder returns. In a note to clients the day before the deal was announced, Tudor Pickering said Anadarko continually came up in meetings as a high-cost standout. Chevron said it can axe about $1 billion a year in operating costs under the transaction, with another $1 billion in savings on capital expenditures.

That may put pressure on other explorers with bloated administrative costs, driving “more meaningful industry consolidation,” Tudor Pickering’s Portillo said. “There’s significant synergy opportunities.”

Spokespeople for Exxon, BP, Shell, WPX, Cimarex, Parsley, Noble, Pioneer, EOG, Occidental and Concho declined to comment or didn’t immediately respond to requests.

— With assistance by Alex Nussbaum, Tina Davis, Ryan Collins, and Kevin Crowley

Fear Grips Norway’s Oil Industry as Political Risk Explodes

Oil companies in Norway may pay some of the highest taxes and wages in the world but they could always count on support in the halls of power.

Then last week the country’s biggest political party pulled out the rug from under that certainty in a dramatic policy shift to abandon support for drilling off the Lofoten islands.

As calls for action against climate change get stronger, concern is mounting within Norway’s biggest industry that the move could open the floodgates and put the country’s oil licensing policies and generous exploration tax incentives at risk ahead of the next election in 2021. Norway, led by Equinor ASA, has been producing oil for almost half a century, but is estimated to have about half its remaining oil and gas still in the ground.

Labor’s shift might not seem like a big deal: the party isn’t currently in government and Lofoten has been off limits for years anyway. Yet it matters because Labor has been a faithful ally of the oil industry for decades, and because it raises the possibility that it will cede more ground on oil policy in coalition talks with other parties.

“This is the first example of climate-policy considerations having a meaningful impact on the oil policy of one of the leading political parties in Norway,” said Klaus Mohn, an economics professor at the University of Stavanger, Norway’s oil capital. “It’s a sort of crossroads.”

Projects Wanted

Norway’s oil and gas output risks a steep drop after 2025 without new finds

Stable and predictable terms have been one of Norway’s main selling points in attracting oil companies. Changes could deepen an expected decline in activity and production in the next decade and bring the Nordic country closer to the end of the oil era that made it so wealthy.

“The stability of the political support to Norway’s oil industry is weakened,” said Jarand Rystad, who heads the country’s top oil consulting firm, Rystad Energy AS. “All of a sudden, you get a real fear of lower activity.”

The firm no longer ranks Norway as the most stable political regime on its internal list of energy-producing countries, Rystad said (see separate story).

Labor’s break frames a broader shift in western Europe’s biggest petroleum-producing nation, where a debate over the oil industry’s future is gaining pace.

So far, drilling opponents have failed to win legal challenges against the country’s oil regulations or to make decisive electoral breakthroughs. The governing Conservative and Progress parties remain staunch supporters of the industry, and Labor vows to back current terms.

Yet Labor’s own youth wing, which scored a big win with Lofoten, wants to shut the oil industry altogether by 2035. It wants to stop license awards and scrap a rule that lets unprofitable companies claim the tax value (78 percent) of exploration expenses in cash rather than in future deductions — an incentive that’s attracted more companies and led to important discoveries. Two of Labor’s potential government partners or backers in parliament, the Socialist Left and Green parties, have similar demands and look set for electoral gains.

The prospect of a compromise spooks oil executives.

Labor’s Lofoten shift is “a frightening development,” said Stale Kyllingstad, chief executive officer of IKM Gruppen AS, one of the domestic industry’s biggest suppliers.

Kjell-Borge Freiberg, Norway’s Petroleum and Energy Minister, called Labor’s decision a “betrayal” of the close to 200,000 people working in the oil industry. “There is a fear for what they might give up next,” Freiberg, a member of the Progress Party, said in a phone interview.

The uncertainty alone will deter companies considering a Norway entry, at a time when the biggest international oil companies are already turning away from Norway, according to Rystad. Norway already lacks big projects and depends on new discoveries to limit the decline in production expected from the mid-2020s.

The bosses of Norway’s oil lobby and biggest industry union reacted with disappointment over the weekend. Yet they said in later interviews they trusted Labor would stand firm on the rest of its oil policy to protect investments and state revenues.

“Anyone who sits down to form a government needs an economic platform,” said Frode Alfheim, the head of the Industry Energy union. “Like it or not, we will remain incredibly dependent on the jobs and the revenue from this industry.”

Chevron mega-deal showcases age of American energy

Bloomberg/Houston/London

For all the ink spilled over climate change and the global energy transition, the world’s biggest energy companies are focusing on where it all began: American oil.

Chevron Corp’s $33bn acquisition of Anadarko Petroleum Corp, announced on Friday, will make the US company the largest producer in the dusty plains of the Permian Basin by giving it control of an oil-rich area twice the size of Los Angeles.

The deal, the industry’s biggest in four years, is fuelling speculation about what arch-rivals Exxon Mobil Corp and Royal Dutch Shell Plc will do next and which other Permian operators are in their sights. Furthermore, it cements the booming oil patch in West Texas and New Mexico as arguably the most dynamic force shaping the global energy market right now. Output there is forecast to grow by millions of barrels in years to come, meaning global producers can’t afford to ignore it.

“It’s a strong message that one of the biggest players in the Permian wants to get even bigger,” Noah Barrett, who helps manage $328bn at Janus Capital Management in Denver. “The only way to do that right now is through M&A. The M&A teams at the other integrateds are certainly sharpening their pencils.”

The Chevron-Anadarko tie-up represents a remarkable turnaround from just a year ago. Coming out the worst price collapse in a generation, oil companies were still pledging capital discipline and vowing to never repeat the overspending seen at the top of almost all previous price cycles.

The newfound humility appeared to hit the right tone, coming at the same time as the industry faced growing pressure from politicians, pressure groups and shareholders to act on climate change. Shell said this year it wants to become the world’s biggest power company. BP Plc is ramping up gas production, which its boss Bob Dudley says is key to replacing coal, a dirtier source of energy.

But after half a decade of cutbacks, and boosted by a Brent crude price that’s up 33% this year, Big Oil is gaining in confidence and looking more favourably at growth.

Exxon is ramping up spending to more than $30bn a year while BP and Total SA also have ambitious plans for new projects.

US shale is attracting more investment dollars than renewables, but so far it’s been dominated by domestic players. Chevron, a bit-part player in the Permian just a few years ago, is poised to become the basin’s top producer and acreage holder once the Anadarko deal is completed later this year.

Total barely has an onshore US presence, nor does Equinor ASA or Eni SpA. BP is the only European oil company that has spent significantly in US shale, paying $10.5bn for the onshore exploration business of BHP Billiton Ltd last year. Shell is in talks to acquire closely held Permian specialist called Endeavor Energy Resources LP, people familiar with the matter said in February.

Giant investor sees profit from fight against climate change

Vapour is released into the sky at a refinery in Wilmington, California. Legal & General Group, one of the world’s biggest investors that oversees $1.3tn, has modelled the climate crisis and sees both risk and a big opportunity, according to Bloomberg. Not only will climate action cost less than expected, but it will make emerging economies more robust. The funds manager anticipates that it can start shifting its investment portfolio now and make extra money during the next few decades – even if politicians keep failing to act on limiting an increase in global temperatures. If they finally do, profits will be even higher. “The cost of transformation will be much more manageable than many people think,” said Nick Stansbury, head of commodities research at the company’s investment management unit. Asset managers are increasingly trying to quantify the risks associated with climate change. While most still rely on external models of the future energy system to make decisions, Legal & General’s work is an indication that some are increasing their scrutiny of the issue.

La pace in Medioriente ha bisogno di energia

Solo poco tempo fa Mike Pompeo, Segretario di Stato Usa, ha concluso il suo giro mediorientale. Un viaggio controverso, che è servito in primis a rassicurare gli alleati nella regione, nell’ottica di tirare le fila della complessa situazione nell’area.

Tra l’altro, Pompeo, è stato in Libano, paese da sempre al centro delle delicate trame politiche mediorientali. Per l’occasione Roudi Baroudi, imprenditore dell’energia libanese, personalità si spicco nel mondo degli affari del Mediterraneo, e apprezzato columnist di vari quotidiani, ha scritto una lettera aperta al Segretario di Stato. Il tema è quello cruciale nella regione. Si parla, appunto dei rapporti tra Israele e Libano sul versante dell’Energia.

«Vari giacimenti di primo piano di idrocarburi sono stati scoperti nel mar Mediterraneo orientale, questi giacimenti offrono un’opportunità storica per migliorare l’economia della zone. Sfortunatamente, il provvido sfruttamento di queste risorse viene rallentato, se non bloccato, perché pochi stati hanno definito i confini marittimi con i loro vicini. Ci sono 12 frontiere tra i sette principali stati costieri» Nota Baroudi. «Solo due di essi sono stati definiti con trattati bilaterali. In una regione che contiene oltre mille miliardi di dollari di petrolio e gas, quindi, l’83 per cento dei confini marittimi rimane irrisolto, con rischi significativi per lo sviluppo in diversi paesi».

Avverte Baroudi: «Fortunatamente le moderne tecnologie di mappatura ora consentono alle applicazioni satellitari di risolvere le controversie offshore, e di farlo con relativa facilità e precisione quasi assoluta». Secondo l’analista libanese «l’argomento più importante» della visita di Pompeo «è stato il progetto degli Stati Uniti per favorire l’accordo sui confini marittimi nel Mediterraneo orientale, in particolare quello tra la Zona Economica Esclusiva tra Libano e Israele». Il grande gioco verte su chi possa sfruttare i giacimenti offshore.

«Nonostante la difficile posizione del loro paese e del sistema di governo imperfetto, i libanesi – secondo Baroudi – esibiscono tremendi poteri di resilienza. Ma questo ciclo non può continuare indefinitamente, specialmente quando il debito nazionale equivale a oltre il 150 percento del Pil. In una recente conferenza di aiuti a Parigi, i paesi donatori hanno chiarito che i loro impegni non si concretizzeranno se e fino a quando il Libano non attuerà riforme radicali, misure anti-corruzione serie e altri passi significativi per mettere ordine dal punto di vista finanziario. Ora, proprio grazie ai nuovi giacimenti offshore potrebbe iniziare una nuova era. Se e quando inizierà la produzione, l’impatto sarà a dir poco rivoluzionario. «Il Libano diventerebbe un esportatore di energia, avrebbe i mezzi per effettuare investimenti senza precedenti in strade, scuole, ospedali. Le entrate del gas potrebbero anche sradicare la povertà e accompagnare le disuguaglianze sociali che forniscono ai gruppi terroristici campi di reclutamento così fertili».

Appunto secondo Baroudi, opinionista autorevole, il prestigio degli Usa nell’area si gioca sulla capacità di mediare tra Libano e Israele sulla questione dei giacimenti di gas offshore. Alcuni, in LIbano, sospettano che lo scopo di Washington non sia quello di facilitare un accordo equo, ma piuttosto di imporne uno sbilanciato che favorisca Israele. «Qualsiasi governo libanese che firmi un tale accordo dovrà affrontare una significativa perdita di legittimità percepita» ammonisce Baroudi. Che sottolinea, appunto, il ruolo costruttivo degli Stati Uniti. «Se l’America agisce come arbitro, un simile esercizio di fair play potrebbe dare all’intera regione la possibilità di disinnescare le tensioni e cambiare direzione D’altra parte, se gli Usa decidessero di agire principalmente come difensore israeliano, non sarà possibile per il governo libanese accettare alcuna proposta». Come si vede, anche nello scacchiere del Mediterraneo dell’Est, la prima discriminante rimane l’energia.

Netherlands Will Soon To Be Home To Europe’s Largest Floating Solar PV Project

Dutch solar developer GroenLeven has announced that it is building a 48 megawatt (MW) floating solar PV project on an old sand extraction site in the Netherlands which, upon completion, will be one of the largest in the world, and the largest in Europe.

The new floating solar park will be built at the Zuidplas in Sellingerbeetse, in the country’s northeast, at an old sand extraction site owned by Kremer Zand en Grind, one of Europe’s leading sand and gravel extracting companies. The electricity generated from the new 48 MW floating solar project will be delivered to Kremer Zand en Grind for its local operations, and being built on an old sand extraction pond opens the door for further development of solar on sand extraction sites.

GroenLeven expects that the new project will deliver the equivalent electricity necessary for powering around 13,000 households and fulfills the company’s existing philosophy of creating solar projects that fulfill a dual function — such as installing solar on rooftops, parking places, landfills, and industrial sites.

Kremer Zand en Grind is also using this new project as a catalyst to relocate a classifying installation for sand extraction located in the Noordplas and a drying installation currently located in Emmen to an industrial park in nearby Groningen-Zuid, to better optimize the company’s electricity usage by bringing the beneficiaries of this new floating solar park closer to hand.

Additionally, Kremer Zand en Grind is also converting its drying installation from gas-fired to an electric dryer, removing a huge amount of gas from its energy mix each year. Further, by co-locating facilities the company will also reduce transport via pipeline of the sand from its extraction site, minimizing disruption to the local communities.

It is also believed that other industries in the surrounding area may benefit from the floating solar project.