Exxon Is in Talks Over Floating LNG Partnership in Israel

Exxon Mobil Corp. is in discussions to build a platform that would expand the export reach of Israel’s biggest natural gas field, according to people familiar with the matter. Israeli gas stocks rose.

The world’s largest publicly-traded oil and gas company is in talks with the firms developing Israel’s Leviathan reservoir to build a floating liquefied natural gas ship, the people said, requesting anonymity because the matter is private. Such a project would allow the Leviathan partners to export to countries not reachable with pipelines and avoid the need to build expensive infrastructure to connect to LNG facilities in Egypt.

It’s possible the discussions ultimately won’t lead to a partnership, the people cautioned. An Exxon representative declined to comment on its intentions in Israel. The company recently made a major gas discovery nearby, off the coast of Cyprus.

“It’s too early to comment on specific development and production timelines” for the Cyprus discovery, the representative said.

Despite considerable gas discoveries in the Eastern Mediterranean region over the past decade, viable export routes have proven tough to find and global energy firms haven’t rushed in. The Leviathan partners have signed deals to meet surging demand in Egypt, Jordan and Israel, but haven’t yet found a way to export to Europe or East Asia.

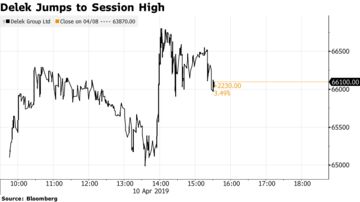

Shares Rise

The partners developing Leviathan, a deep-sea find of about 600 billion cubic meters — at the time it was found, the biggest underwater gas discovery in a decade — have bookmarked the next phase of the reservoir’s development for export deals and are examining ways to reach markets outside the region. Delek Drilling LP, the biggest shareholder in the Leviathan field, is looking into several options, such as buying a stake in one of Egypt’s LNG sites.

Delek Group Ltd., controlled by billionaire Yitzhak Tshuva and largest shareholder of Delek Drilling, climbed as much as 6.5 percent on the news. Ratio Oil Exploration 1992 LP, which owns a 15 percent stake in the Leviathan project, gained as much as 4.6 percent.

The talks with Exxon are the latest sign that an unofficial energy boycott on Israel, imposed by leading Arab countries, is fading. Energy majors that partner with big Arab firms have hesitated to do business with Israel in the past, for fear of risking ties with states that control some of the world’s biggest energy reserves and have been hostile toward Israel until now.

Those concerns seem to be dissipating. Israel and Persian Gulf states have found common cause against Iran, leading some Arab leaders, such as Saudi Crown Prince Mohammed Bin Salman, to break longstanding diplomatic taboos on Israel. Covert trade with the Arab world, mainly involving Israel’s technology sector, also has grown.

For Exxon, expanding into Israel would reflect the company’s growing ambitions in the East Med, an area that straddles Egyptian, Israeli, Lebanese and Cypriot waters. Exxon established a foothold in the region in February, when it found an offshore reservoir in Cypriot waters that’s about one-third the size of Leviathan.

Exxon recently spoke with Israeli Energy Minister Yuval Steinitz about participating in an upcoming tender for new offshore drilling blocs, according to people familiar with the matter.

https://www.bloomberg.com/amp/news/articles/2019-04-10/exxon-is-said-in-talks-over-floating-lng-partnership-in-israel?__twitter_impression=true