La fronde anti-éoliennes prend de l’ampleur

ENQUÊTE – Le gouvernement souhaite doubler le nombre d’éoliennes sur le territoire dans les cinq prochaines années. Mais la contestation s’intensifie et réunit des opposants de tous bords.

Après les McDonald’s et les champs d’OGM, la prochaine cible des écologistes ou des zadistes sera-t-elle l’éolien? En juin, un feu criminel détruisait une éolienne et en endommageait une autre à Marsanne, dans la Drôme. L’attaque a été revendiquée mi-juin par un site libertaire précisant «s’attaquer aux dominations». Du bourgeois au militant mélenchoniste en passant par l’anarchiste, le pêcheur et le châtelain, l’opposition à l’éolien est «de plus en plus composite», affirme Fabien Bouglé, porte-parole du collectif d’opposants Touche pas à nos îles! en guerre contre le projet de parc éolien au large de l’île de Noirmoutier, en Vendée.

Certes, cette opposition a historiquement débuté chez des pronucléaires situés bien à droite, «mais ça change», souligne cet élu versaillais, spécialiste du marché de l’art, qui témoigne avoir assisté à une lecture sur le sujet dans une «librairie anar de gauche» à Paris, et qui prophétise «une grande révolte populaire anti-éoliennes». D’autant que semble s’opérer une mutation: la contestation, jusque-là cantonnée aux citoyens et aux associations anti-éoliennes, trouve désormais des voix et des relais dans le monde politique pour porter le combat.

Ainsi Xavier Bertrand, ancien ministre du Travail et actuel président de la région des Hauts-de-France, qui a lancé fin juin un observatoire de l’éolien afin de mieux contrôler l’expansion des parcs dans sa région, qui «défigure complètement les paysages» et «coûte les yeux de la tête». Ou encore ces dix députés, tant de la majorité que de l’opposition, qui ont signé une tribune, «Stop aux nouvelles éoliennes!», dans nos éditions du 20 juin dernier.

Projet «antidémocratique»?

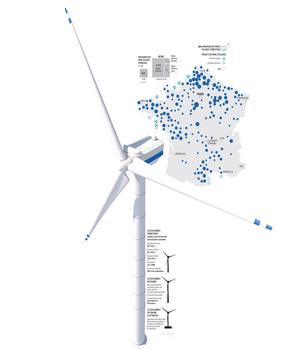

La France constitue aujourd’hui le quatrième parc d’Europe derrière l’Allemagne, l’Espagne et la Grande-Bretagne. Sa proportion d’électricité éolienne représente moins de 5 % de sa consommation mais, d’ici à 2023, les éoliennes terrestres devraient doubler, passant de 7300 à quelque 15.000. «C’est le deuxième gisement de vent d’Europe et la deuxième façade maritime. Le potentiel est considérable», selon Pauline Le Bertre, déléguée générale de France Énergie éolienne (FEE).

On compte 70 % de recours contre les permis de construire devant les tribunaux administratifs, contre 50 % il y a cinq ans

Si l’Allemagne a depuis longtemps compris «la nécessité impérative d’avoir une transition énergétique, en France, de nombreuses associations jouent sur les angoisses des gens, propageant des idées reçues». Le degré d’opposition à l’éolien serait, selon elle, unique en Europe, lié à notre historique avec le nucléaire.

De fait, malgré le discours politique français très volontariste sur le sujet, malgré les sondages favorables à l’éolien menés auprès des Français, l’installation des éoliennes suscite de plus en plus d’opposition. On compte 70 % de recours contre les permis de construire devant les tribunaux administratifs, contre 50 % il y a cinq ans. Une perte de temps pour les promoteurs: la mise en route d’un parc est désormais d’environ neuf ans, contre quatre pour l’Allemagne.

Pour accélérer le processus, le gouvernement a décidé de supprimer le premier degré de juridiction, le tribunal administratif, pour passer directement à la cour administrative d’appel. Un projet de décret est actuellement en consultation devant le Conseil d’État. Cela se pratique déjà pour les projets éoliens en mer, les multiplexes de cinéma et les supermarchés. Un projet «antidémocratique» pour Fabien Bouglé, et qui, ces derniers mois, mobilise et durcit plus encore le front anti-éolien.

Biodiversité

Les associations d’opposants s’offusquent aussi d’un décret paru le 11 juillet qui permet de moderniser les parcs existants sans reprendre de zéro toutes les études d’impact. Que reprochent ces opposants à l’éolien? Sa laideur, sa proximité avec des habitations et des monuments historiques, ses nuisances sonores, ses lumières «aveuglantes», des installations entachées de multiples prises illégales d’intérêt de la part des élus. Les arguments sont multiples. Et parfois écoutés.

Des éoliennes ne seront ainsi pas installées en arrière-plan du paysage du Mont-Saint-Michel, pas plus que du côté du pont du Gard. Pauline Le Bertre, elle, indique qu’en France «les restrictions d’installation sont les plus élevées d’Europe. On multiplie les études d’impact liées à la biodiversité, le patrimoine, les habitations.» À l’entendre, une éolienne implantée à 500 mètres d’une habitation, le minimum réglementaire, «fait un bruit semblable à celui d’un frigidaire». Elle vante la compétitivité du mégawatt éolien, 64 euros contre 110 pour le nucléaire dernière génération. Inversement, Karine Poujol, à la tête de l’association Gardez les caps, considère que les 64 éoliennes prévues en baie de Saint-Brieucprovoqueront la mort de la biodiversité sous-marine, alors même que la zone est protégée Natura 2000. Elle anticipe un bruit «semblable à celui d’un décollage d’avion».

Loïk Le Floch-Prigent, ancien PDG d’Elf Aquitaine, défend les coquilles Saint-Jacques du cap Fréhel, qui pourraient être «très affectées» par ces installations fixées par 42 mètres de fonds. L’ancien industriel se défend de jouer pour le camp des pronucléaires, lui qui a «toujours défendu le fait qu’il fallait diversifier», rapporte-t-il au Figaro. Il met en doute cette politique qui «pénalise notre compétitivité en augmentant nos importations de matériel: 95 % des investissements de l’éolien viennent d’Allemagne, du Danemark, d’Inde ou de Chine, tandis que deux tiers des exploitants viennent d’ailleurs». Ce printemps, la Cour des comptes affirmait que «le tissu industriel français a peu profité du développement des énergies renouvelables». Malgré des moyens considérables, qui se sont élevés en 2016 à 5,3 milliards d’euros. La prévision de dépense publique en 2023, elle, est de 7,5 milliards d’euros.