Opec withdrawal fits Qatar’s LNG strategy, says US finance attache

Qatar’s recent decision to withdraw its membership from the Organisation of the Petroleum Exporting Countries (Opec) is a business decision that supports the country’s development strategy for its liquefied natural gas (LNG) sector, industry experts agreed during the Euromoney Conference held in Doha on Sunday.

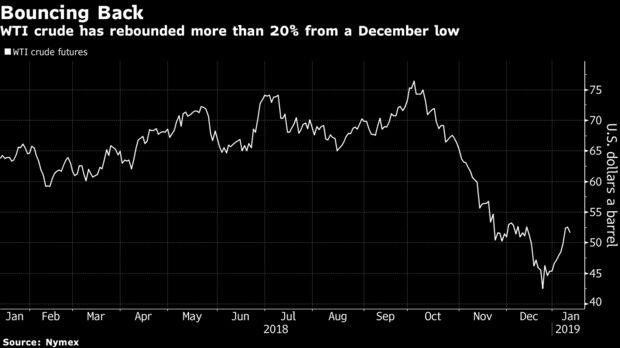

Qatar is Opec’s 11th-biggest oil producer. Lesley Chavkin, the US Department of the Treasury financial attaché to Qatar and Kuwait, pointed out that Qatar’s total output accounts for “only 2%.”

“Qatar is not a behemoth in Opec, and I think it (withdrawal from Opec) fits with the strategy to focus the resources on LNG. That seems to be the future of Qatar’s energy industry,” Chavkin said during the panel discussion titled ‘Qatar’s Economy — New Directions, New Opportunities’.

On the global market, Chavkin also said that Qatar is expanding its reach, veering towards the Asia Pacific region. She noted that Qatar may have to look into short-term contracts with its Asian buyers.

“Obviously, it’s no surprise that the demand is coming from the Asia Pacific region. We have China aggressively moving from coal to gas…moving forward, it’s going to be Asian-focused.

“What I think is a kind of interesting space to watch is LNG contracts. So, Asian buyers tend to prefer buying LNG on spot or short-term basis. LNG contracts here tend to be longer term, and Qatar has flexibility in adjusting some of its longer term contracts to maintain market share but that’s something interesting that we would be watching, going forward,” Chavkin explained.

Mohamed Barakat, the managing director of US-Qatar Business Council, said he agrees with Qatar’s decision to withdraw its membership from Opec, “because this is a business-focused decision.”

“Qatar is in the gas business and its oil production doesn’t affect the market that much as countries like Saudi Arabia,” Barakat said.

He added: “Qatar’s decision to increase its gas production will definitely increase the support and supplies that Qatar can provide globally, knowing that from a US perspective, Qatar has provided a lot of LNG to US allies, supporting them, and helping them to be more independent with a reliable partner in Qatar — that would help advance more the business interests globally in Qatar, as well.”

Alexis Antoniades, the director of International Economics at Georgetown University — Qatar, emphasised that the decision to withdraw Qatar’s Opec membership is a business decision and was not politically motivated.

“I don’t see any political decision behind it… this is a business decision. We have no role in Opec… we are in the LNG industry and not the oil sector. It makes sense for us to withdraw there, and it makes sense for us to figure out what is it that we are going to do well, and focus our time and resources on that,” Antoniades said.

“Qatar is not a behemoth in Opec, and I think it (withdrawal from Opec) fits with the strategy to focus the resources on LNG. That seems to be the future of Qatar’s energy industry,” Chavkin said during the panel discussion titled ‘Qatar’s Economy — New Directions, New Opportunities’.

On the global market, Chavkin also said that Qatar is expanding its reach, veering towards the Asia Pacific region. She noted that Qatar may have to look into short-term contracts with its Asian buyers.

“Obviously, it’s no surprise that the demand is coming from the Asia Pacific region. We have China aggressively moving from coal to gas…moving forward, it’s going to be Asian-focused.

“What I think is a kind of interesting space to watch is LNG contracts. So, Asian buyers tend to prefer buying LNG on spot or short-term basis. LNG contracts here tend to be longer term, and Qatar has flexibility in adjusting some of its longer term contracts to maintain market share but that’s something interesting that we would be watching, going forward,” Chavkin explained.

Mohamed Barakat, the managing director of US-Qatar Business Council, said he agrees with Qatar’s decision to withdraw its membership from Opec, “because this is a business-focused decision.”

“Qatar is in the gas business and its oil production doesn’t affect the market that much as countries like Saudi Arabia,” Barakat said.

He added: “Qatar’s decision to increase its gas production will definitely increase the support and supplies that Qatar can provide globally, knowing that from a US perspective, Qatar has provided a lot of LNG to US allies, supporting them, and helping them to be more independent with a reliable partner in Qatar — that would help advance more the business interests globally in Qatar, as well.”

Alexis Antoniades, the director of International Economics at Georgetown University — Qatar, emphasised that the decision to withdraw Qatar’s Opec membership is a business decision and was not politically motivated.

“I don’t see any political decision behind it… this is a business decision. We have no role in Opec… we are in the LNG industry and not the oil sector. It makes sense for us to withdraw there, and it makes sense for us to figure out what is it that we are going to do well, and focus our time and resources on that,” Antoniades said.

MILAN – About a decade ago, the Commission on Growth and Development (which I chaired) published a report that attempted to distill 20 years of research and experience in a wide range of countries into lessons for developing economies. Perhaps the most important lesson was that growth patterns that lack inclusiveness and fuel inequality generally fail.

The reason for this failure is not strictly economic. Those who are adversely affected by the means of development, together with those who lack sufficient opportunities to reap its benefits, become increasingly frustrated. This fuels social polarization, which can lead to political instability, gridlock, or short-sighted decision-making, with serious long-term consequences for economic performance.

There is no reason to believe that inclusiveness affects the sustainability of growth patterns only in developing countries, though the specific dynamics depend on a number of factors. For example, rising inequality is less likely to be politically and socially disruptive in a high-growth environment (think a 5-7% annual rate) than in a low- or no-growth environment, where the incomes and opportunities of a subset of the population are either stagnant or declining.

The latter dynamic is now playing out in France, with the “Yellow Vest” protests of the last month. The immediate cause of the protests was a new fuel tax. The added cost was not all that large (about $0.30 per gallon), but fuel prices in France were already among the highest in Europe (roughly $7 per gallon, including existing taxes).

Although such a tax might advance environmental objectives by bringing about a reduction in emissions, it raises international competitiveness issues. Moreover, as proposed, the tax (which has now been rescinded) was neither revenue-neutral nor intended to fund expenditures aimed at helping France’s struggling households, especially in rural areas and smaller cities.

In reality, the eruption of the Yellow Vest protests was less about the fuel tax than what its introduction represented: the government’s indifference to the plight of the middle class outside France’s largest urban centers. With job and income polarization having increased across all developed economies in recent decades, the unrest in France should serve as a wake-up call to others.

y most accounts, the adverse distributional features of growth patterns in developed economies began about 40 years ago, when labor’s share of national income began to decline. Later, developed economies’ labor-intensive manufacturing sectors began to face increased pressure from an increasingly competitive China and, more recently, automation.

For a time, growth and employment held up, obscuring the underlying job and income polarization. But when the 2008 global financial crisis erupted, growth collapsed, unemployment spiked, and banks that had been allowed to become too large to fail had to be bailed out to prevent a broader economic meltdown. This exposed far-reaching economic insecurity, while undermining trust and confidence in establishment leaders and institutions.

To be sure, France, like a number of other European countries, has its share of impediments to growth and employment, such as those rooted in the structure and regulation of labor markets. But any effort to address these issues must be coupled with measures that mitigate and eventually reverse the job and income polarization that has been fueling popular discontent and political instability.

So far, however, Europe has failed abysmally on this front – and paid a high price. In many countries, nationalist and anti-establishment political forces have gained ground. In the United Kingdom, widespread frustration with the status quo fueled the vote in 2016 to leave the EU, and similar sentiment is now undermining the French and German governments. In Italy, it contributed to the victory of a populist coalition government. At this point, it is difficult to discern viable solutions for deepening European integration, let alone the political leadership needed to implement them.

The situation is not much better in the United States. As in Europe, the gap between those in the middle and at the top of the income and wealth distribution – and between those in major cities and the rest – is growing rapidly. This contributed to voters’ rejection of establishment politicians, enabling the victory in 2016 of US President Donald Trump, who has since placed voter frustration in the service of enacting policies that may only exacerbate inequality.

In the longer term, persistent non-inclusive growth patterns can produce policy paralysis or swings from one relatively extreme policy agenda to another. Latin America, for example, has considerable experience with populist governments that pursue fiscally unsustainable agendas that favor distributional components over growth-enhancing investments. It also has considerable experience with subsequent abrupt shifts to extreme market-driven models that ignore the complementary roles that government and the private sector must play to sustain strong growth.

Greater political polarization has also resulted in an increasingly confrontational approach in international relations. This will hurt global growth by undermining the world’s ability to modify the rules governing trade, investment, and the movement of people and information. It will also hamper the world’s ability to address longer-term challenges like climate change and labor-market reform.

But to go back to the beginning, the main lessons from experience in developing and now developed economies are that sustainability in the broad sense and inclusiveness are inextricably linked. Moreover, large-scale failures of inclusion derail reforms and investments that sustain longer-term growth. And economic and social progress should be pursued effectively – not with a simple list of policies and reforms, but with a strategy and an agenda that involves careful sequencing and pacing of reforms and devotes more than passing attention to the distributional consequences.

The hard part of constructing inclusive growth strategies is not knowing where you want to end up so much as figuring out how to get there. And it ishard, which is why leadership and policymaking skill play a crucial role.