السعودية – الصين: شراكة نفطية ترسم معالم عصر جديد في الطاقة

يمثل #التعاون النفطي بين السعودية والصين أحد أهم الشراكات الاستراتيجية في العصر الحديث، إذ يجمع بين أكبر مصدر للنفط في العالم وأكبر مستورد له. إلا أن هذا التعاون لا يقتصر على تجارة النفط وحدها، بل يشمل استثمارات مشتركة تهدف إلى تعزيز العلاقات الاقتصادية الثنائية، خصوصاً مع توسع “#أرامكو السعودية” في السوق الصينية.

منصة “مرجان”!

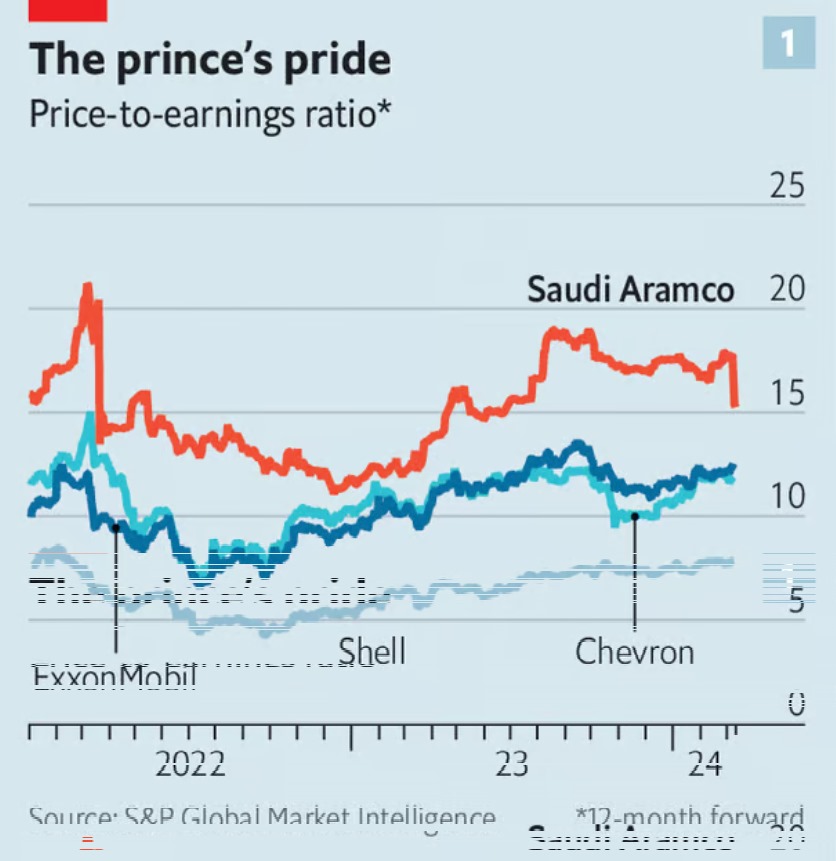

بلغت #الاستثمارات الصينية في السعودية 16,8 مليار دولار في عام 2023، في مقابل 1,5 مليار دولار في عام 2022، استناداً إلى بيانات بنك الإمارات دبي الوطني. في هذا الإطار، يوضح الدكتور خالد رمضان، الخبير النفطي ورئيس المركز الدولي للدراسات الاستراتيجية بالقاهرة، لـ “النهار” أن هذا ا#لتعاون النفطي السعودي – الصيني يؤثر إيجاباً في #أسواق الطاقة العالمية، “وما منصة ’مرجان‘ النفطية البحرية التابعة لأرامكو في الصين إلا ترجمة فعلية لهذا التعاون”، وستستخدم لزيادة الإنتاج السنوي لحقل المرجان النفطي إلى 24 مليون طن.

وتعد منصة “مرجان” أثقل منصة نفط وغاز بحرية في الصين مخصصة للأسواق الخارجية، وواحدة من أكبر المنصات في العالم، فهي أطول من مبنى مكون من 24 طابقًا، وتعادل مساحة سطحها 15 ملعب كرة سلة، ويمكنها جمع ونقل 24 مليون طن من النفط و7,4 مليارات متر مكعب من الغاز سنويًا.

شريكة في التنمية

يضيف رمضان: ” أبرمت أرامكو السعودية في عام 2023 صفقات بقيمة 8 مليارات دولار مع شركاء صينيين في قطاعي المنبع أي الاستكشاف والإنتاج، والمصب أي التكرير والتوزيع”. إلى ذلك، توظف نظرتها المتفائلة إلى إمكانات النمو في الصين على المدى الطويل، والفرص عالية الجودة، “من أجل توسيع عملياتها المتكاملة في قطاع الصناعات التحويلية الصينية، والتي يمثل الاستثمار فيها أهمية استراتيجية لنمو أعمال أرامكو في آسيا”.

يلفت رمضان إلى أن دور أرامكو يتجاوز الاستثمار، “لأنها تريد أن تكون شريكاً رئيسياً في التنمية الاقتصادية في الصين، والاستفادة من الفرص الجديدة التي تلوح في الأفق، من خلال شراكات استراتيجية تعزز وجودها في قطاع الصناعات التحويلية في الصين، بما فيها المواد الكيميائية والمواد المركبة المتقدمة والمواد غير المعدنية”.

وهكذا، تظل الصين محورية في استراتيجية أرامكو لتنويع محفظتها، لتشمل منتجات كيميائية أكثر تخصصًا وعالية القيمة، خصوصاً أن الصين تمثل 40 في المئة من مبيعات المنتجات الكيميائية العالمية.

تعزيز سلاسل التوريد

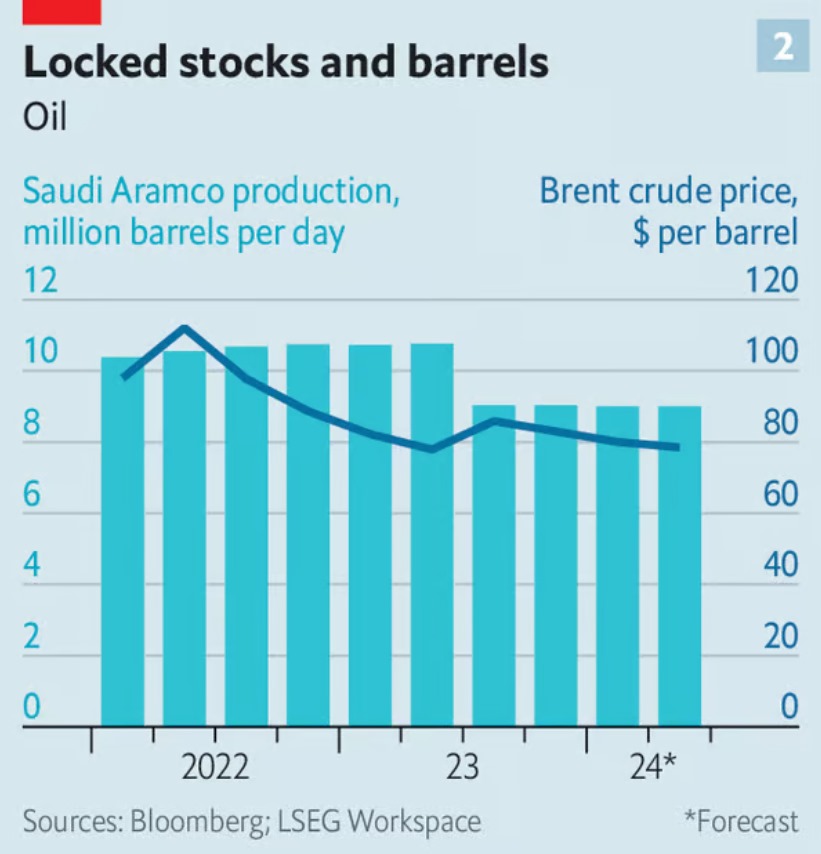

الصين ثاني أكبر اقتصاد في العالم، لذا تعد أكبر مستورد للنفط الخام، إذ تستهلك 14 مليون برميل يوميًا، تليها أوروبا بنحو 12,8 مليون برميل يوميًا. من ناحية أخرى، تعد السعودية أكبر مصدر للنفط الخام في العالم، تليها روسيا وكندا والنرويج ونيجيريا.

وانطلاقاً من هذا الواقع، “سهل أن نرى كيف يمنح توسيع التعاون النفطي بين الصين والسعودية الأسواق استقرارًا أكبر، ويعزز أمان سلاسل الإمداد النفطية، ويزيد فرص المنافسة في الأسواق العالمية”، بحسب ما يقول الخبير النفطي الدولي رودي بارودي.

ويضيف لـ”النهار”: “بالنسبة إلى السعوديين، سيضمنون شريكاً استراتيجياً طويل الأمد، لن يشتري النفط الخام فحسب، بل يستثمر أيضًا في سلسلة النفط اللاحقة، من المصافي إلى مصانع البتروكيماويات”. فأرامكو السعودية، أكبر شركة نفط في العالم، مستثمر كبير في مشروع “رونغشينغ سينوبيك فوجيان” للتكرير والبتروكيماويات (Rongsheng Sinopec Fujian Refining & Petrochemical venture)، وفي شركتين كبيرتين للبتروكيماويات هما “هينغلي” (Hengli Petrochemical) و”رونغشينغ” (Rongsheng Petrochemical). وتفاوض أرامكو لشراء 10 في المئة في “هينغلي”، وتسعى لإبرام صفقات مماثلة مع شركتين صينيتين أخريين، بعدما أبرمت صفقة منفصلة قيمتها 3,4 مليارات دولار لشراء حصة في شركة “رونغشينغ” في العام الماضي.

تحالف مؤثر

في الضفة الأخرى، استثمرت الصين مليارات الدولارات في السعودية، “حيث دخلت الشركات الصينية على خطّ مشاريع سعودية واسعة النطاق تركّزت في معظمها في التكرير والبنية الأساسية للغاز”، بحسب بارودي، الذي يضيف: “من شأن التعاون الطويل الأجل بين البلدين أن يعيد تشكيل أجزاء من المشهد النفطي والبتروكيماوي العالمي”.

ويؤكد الخبير النفطي الدولي أن أرامكو السعودية مستثمر كبير في صناعة الهيدروكربون في الصين، “والجانبان يركزان جهودهما على توسيع مصانع إنتاج السوائل وتحويلها إلى كيماويات في مصفاة الجبيل بالسعودية، وفي وحدة البتروكيماويات في نينغبو تشونجين بالصين”.

ويرى بارودي أن هذا التطوّر في العلاقة التصنيعية والتحويلية هو “نتاج علاقة استراتيجية ديبلوماسية سعودية – صينية، بدأت تحاك قبل أكثر من ثلاثة عقود، لا تقتصر على التجارة والاستثمارات المتبادلة، بل تتعداها إلى تحالف تنعكس آثاره على الاقتصاد العالمي، ما من شأنه أن يقلل من تأثير أي تباطؤ اقتصادي في المستقبل، وأن يحمي أسواق الهيدروكربون والبتروكيماويات”.

إلى جانب ذلك، يعزز التعاون بين السعوديين والصينيين التحول العالمي في مجال الطاقة، بفضل التوافق في الرؤى التنموية بين البلدين. فرؤية “السعودية 2030” ومبادرة “الحزام والطريق” الصينية تستهدفان إضافة المزيد من الاستثمارات في الطاقة المتجددة. ومن هنا، تستهدف أرامكو الاستفادة من الطلب المتزايد على الصناعات الخضراء الناشئة في الصين، “ليتطوّر التعاون الصيني – السعودي في مجال الطاقة من مجرد تعاون في مصادر طاقية تقليدية ليشمل قطاع الطاقة الجديدة”، بحسب رمضان.

شراكة تبادلية

يقول بارودي إن هذا التعاون يرتقي يوماً بعد يوم إلى مستوى الشراكة التبادلية، “فالفوائد متبادلة، ويعمل كل من الطرفين على تنويع إيراداته، وخفض إنفاقه الإنتاجي”، مذكراً بأن هذا التعاون “يدعم قدرة البلدين على تحقيق استقرار الاقتصاد العالمي، إذ يبشّر بتغييرات مالية ضخمة”.

فمحتمل جداً أن تبدأ السعودية بقبول اليوان الصيني، من بين عملات آسيوية أخرى، بوصفه عملة معتمدة في التبادلات النفطية. وهذا، برأي بارودي، يمنح الصين والسعودية مزايا اقتصادية كبيرة، خصوصاً أن المملكة جادة في مسيرة تنويع مصادر اقتصادها، والخروج من دائرة الاعتماد الكلي على الإيراد النفطي”.

يضيف بارودي: “إن تحققي المملكة هذا الهدف سيشكل نقطة تحوّل أساسيّة في سياستها الاقتصادية عموماً، والنفطية خصوصاً، إذ ستكمل تحررها من قيود البترو-دولار بعد اتفاقية مع الولايات المتحدة دامت 50 عاماً، وبعد دخولها مع الصين في مجموعة الـ ’بريكس‘ التي وضعت نصب عينيها الوقوف في وجه هيمنة الدولار الأميركي على الاقتصاد العالمي”.